Executive Summary

Earlier this month, New York became the first U.S. state to offer all but its wealthiest residents free tuition not only at its public community colleges, but also at public four-year institutions in the state. The new program, called the Excelsior Scholarship, doesn’t make college completely free, nor is it without significant restrictions. [1] Still, the passage of this legislation demonstrates the growing strength of the free college movement in the United States.

The free college movement in the U.S. is typically associated with liberal and progressive politics and motivated by concerns about rising inequality and declining investments in public goods like education. Americans are thus sometimes surprised to hear the story of the end of free college in England, in which progressives built upon very similar motivations to move policy in the complete opposite direction.

Until 1998, full-time students in England could attend public universities completely free of charge. But concerns about declining quality at public institutions, government mandated caps on enrollment, and sharply rising inequality in college attainment led to a package of reforms which began in 1998, including the introduction of a modest tuition fee. Two decades later, most public universities in England now charge £9,250—equivalent to about $11,380, or 18 percent more than the average sticker price of a U.S. public four-year institution. [2] The typical English bachelor’s degree recipient is now expected to graduate with around £44,000 (approximately $54,918) in student loan debt, more than twice the average for graduates who borrow at U.S. four year institutions. [3]

Has this restructuring of higher education finance over the last 20 years led the English system backwards or forwards in terms of improving quality, quantity, and equity in higher education? In this report, Evidence Speaks contributor Judith Scott-Clayton teams up with two experts on British higher education—Richard Murphy and Gillian Wyness—to examine the consequences of ending free college in England, and consider what lessons may be drawn for the U.S. policy conversation.

Though it is impossible to know how trends would have evolved absent the 1998 reforms, we show that at a minimum, ending free college in England has not stood in the way of rising enrollments, and institutional resources per student (one measure of quality) have increased substantially since 1998. Moreover, after many years of widening inequality, socioeconomic gaps in college attainment appear to have stabilized or slightly declined.

The English experience thus suggests that making college free is hardly the only way to increase quantity, quality, and equity in higher education. Indeed, the story we tell here shows how a free system can eventually stand in the way of these goals. Rather than looking to emulate the English model of the 1990s, the U.S. might instead consider emulating some key features of the modern English system that have helped moderate the impact of rising tuition, such as deferring all tuition fees until after graduation, increasing liquidity available to students to cover living expenses, and automatically enrolling all graduates in an income-contingent loan repayment system that minimizes both paperwork hassle and the risk of default.

Challenges during England’s free college era [4]

Prior to 1998, public universities in England were fully funded by local education agencies and the national government such that college was completely tuition-free for full-time domestic students. [5] To help cover living expenses while enrolled, low-income students could apply for grants, and all students could obtain small government loans to be repaid via mortgage-style payment plans after graduation.

From a U.S. perspective, the English system prior to 1998 might appear on its surface to be practically utopian (indeed, that is how it appeared to one of us as a U.S. undergraduate studying abroad in London around the time of the reform). And perhaps for a time it was, at least for those who qualified academically for college admission, and as long as not too many people wanted to go.

As demand for college-educated workers increased during the late 1980s and 1990s, however, college enrollments rose dramatically and the free system began to strain at the seams. Government funding failed to keep up, and institutional resources per full-time equivalent student declined by over 25 percent in real terms between 1987 and 1994. [6] In 1994, the government imposed explicit limits on the numbers of state-supported students each university could enroll. Despite these controls, per-student resources continued to fall throughout the 1990s. By 1998, funding had fallen to about half the level of per-student investment that the system had provided in the 1970s.

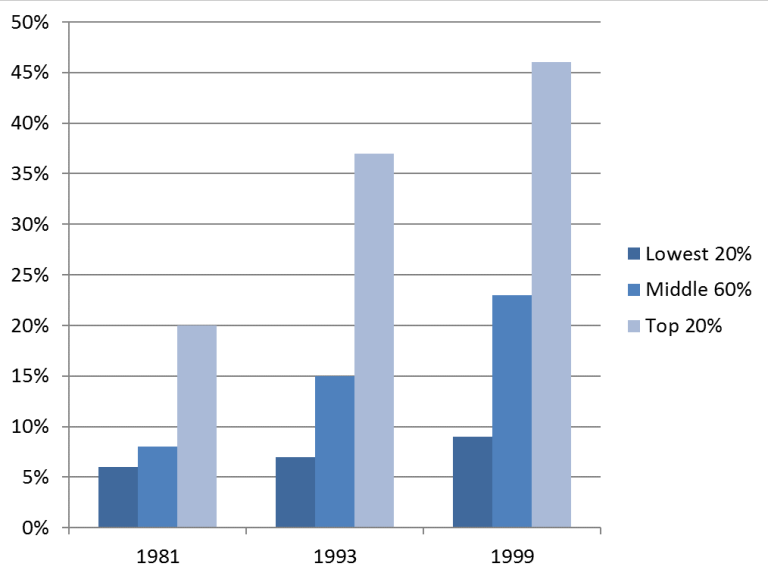

In addition, even as enrollments rose overall, low-income students fell further and further behind despite the zero price tag. Figure 1 shows that the gap in degree attainment between high- and low-income families more than doubled during this period, from 14 to 37 percentage points [7] (note that in the highly structured English curriculum, enrollment and completion are almost the same thing, in contrast to the U.S. [8]).

Figure 1. Percent with BA/BSc degree by age 23, by family income

Source: Blanden & Machin (2013), based on national longitudinal cohort surveys. [9]

To summarize, one of the main challenges of the free college era in England was insufficient funding to support the “massification” of higher education. As competition for spots increased, it appeared that the free college tuition subsidy was increasingly going to those from the richest backgrounds.

The 1998 reform: progressive economic arguments for introducing tuition [10]

It was against this backdrop that the National Committee of Inquiry into Higher Education released the Dearing Report in 1997, which called for new tuition fees supported by an expanded and revised system of student loans. [11] The fees of up to £1,000 per year would be means-tested such that low-income students would face no change in price. At the same time, the government would implement a new income-contingent loan (ICL) system that enabled all students to access significantly more funds while enrolled, with zero-real-interest loans paid back as a fraction of income only after graduates begun earning above a minimum level. [12]

It should come as no surprise that the idea of shifting costs from taxpayers to students would appeal to conservative lawmakers concerned about public expenditures. But some progressive policymakers—primarily concerned with caps on enrollment, declining quality, and rising inequality—also made the case against keeping college completely free.

The progressive argument for introducing fees and expanding loans had several components. [13] First, complete reliance on public funding meant universities were under constant pressure to limit enrollments, reduce per-student expenditures, or both (with higher-achieving students, and more elite institutions, typically most insulated from these consequences). Meanwhile, because of substantial inequality in pre-college achievement, the main beneficiaries of free college were students from middle- and upper-class families—who, on average, would go on to reap substantial private returns from their publicly-funded college degrees. Finally, cost remained a major barrier for low-income students even in the absence of tuition fees: many still struggled to afford necessary expenses for food, housing, books, and transportation. Yet prioritizing free tuition for all students left little room in the budget to provide additional supports for low-income students.

By charging tuition, progressives argued that the system could bring in more resources from students who could afford to pay, while enabling any given level of public subsidies to go further by targeting assistance to the neediest (including efforts to reduce pre-college disparities in achievement). Further, the new income-contingent loan system would enable students to safely tap into their future expected earnings so they could more easily afford the full cost of attendance, including basic costs of living while enrolled.

Progressives hoped that the proposed reforms would improve quality, allow for higher levels of enrollment, and reduce educational inequity. Critics, however, feared that the modest initial £1,000 fee was just the proverbial camel’s nose under the tent: that fees would inevitably rise and public funding would inevitably fall, ultimately undermining progressive goals.

Consequences of the reform for college costs and student aid

From the student perspective, what were the practical effects of the reform? In at least one sense, the worriers were right: the 1998 reform fundamentally changed the structure of English higher education finance, and the numerous subsequent reforms it enabled in tuition and financial aid policy have led to an entirely new landscape for new students to navigate. These changes included substantial increases in tuition fees, to £3,000 in 2006 and £9,000 in 2012—though beginning in 2006, these fees were not charged “up-front” but were automatically covered for all students via an income-contingent loan. Table 1 provides a timeline of key aspects of the 1998 and subsequent reforms, which included major changes to grant and loan assistance as well.

Table 1. Key features of English postsecondary finance over time

| Pre- 1998 | – No tuition fees for full-time domestic students.

– Means-tested “maintenance” grants up to £2,000 per year for living expenses – Zero real interest rate maintenance loans up to £2,000, to be repaid in 60 monthly installments |

| 1998-99 | – Means-tested upfront tuition fee introduced, up to £1,000 per year

– Loans were expanded for all income levels (with more for low-income) and mortgage-style repayment system replaced with income-contingent repayment system |

| 1999-00 | – Means tested maintenance grants eliminated |

| 2004-05 | – Means tested maintenance grants up to £1,000 reintroduced |

| 2006-07 | – Tuition fee increased to £3,000 and means-testing removed, but fee not charged up-front; all students pay after graduation via income contingent loan system

– Means tested maintenance grants increased up to £2,700 – Universities instructed to use at least 10 percent of fee revenue for additional grants (bursaries) for low-income students |

| 2008-09, 2009-10 | – Expansion of maintenance grants & loans to middle- and higher-income students

– Means-tested maintenance grants increased up to £2,900 |

| 2011-12 | – Means-tested maintenance grants increased to £3,250 |

| 2012-13 | – Maximum tuition fee raised to £9,000, with maximum in subsequent years to increase with inflation

– Maximum allowable student numbers (enrollment caps) to be phased out with complete elimination by 2015-16 – Loan repayment threshold raised to £21,000 per year, indexed to wages – Interest rate on income contingent loans set at maximum of Retail Price Index (RPI) plus 3 percent for graduates earning above £41,000 per year (and tapered to RPI for graduates earning £21,000 per year); payments stop when balance is paid, or after 30 years, whichever comes first. |

Source: Students Loans Company (2012), Smith (2004). [14]

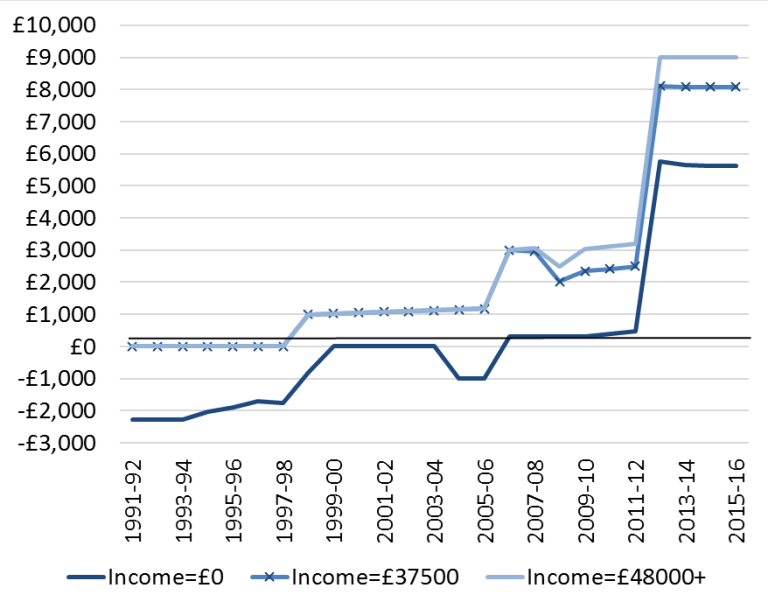

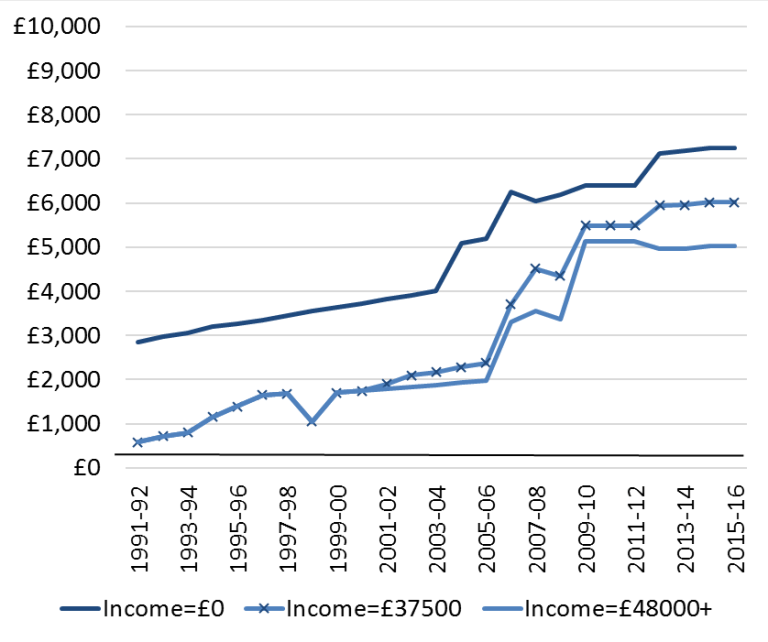

We can summarize the practical effects for students along two key dimensions. First, how did the net price of university (tuition minus grant aid) change over time for students at different income levels? Second, how did net liquidity (grants, plus maintenance loans, minus any upfront fees) change over time, by family income? [15]

Figure 2 plots net tuition prices over time by family income, while Figure 3 plots net liquidity. These figures provide three insights. First, they confirm that the modest effects of the initial 1998 reform paved the way for much bigger changes in 2006 and 2012. Second, the reforms increased students’ liquidity—the amount of cash they could receive to support living expenses while enrolled—almost as dramatically as they increased tuition fees. Students from the lowest income groups have access to over £7k worth of liquidity for living expenses per year, in addition to the tuition fee loan, roughly £2k more than students from the highest income group. Third, the progressivity of the pricing structure has not changed much in the years since the initial reform; low-income students have always paid less, but prices and liquidity have risen similarly across income groups. [16]

Figure 2. Net price (fees-grants) by family income, over time

Figure 3. Net liquidity (grants+loans-upfront fees) by family income, over time

Source: Authors’ calculations using data from Student Loans Company, 1991-2015. [17]

Table 2 further summarizes, in a broad sense, who pays and who benefits under England’s new model of higher education finance. By 2012-13, the total resources flowing into higher education had increased dramatically, with graduates themselves expected to shoulder more than half of the cost of their education (£7.9 billion versus £5.9 billion in taxpayer support). Note that taxpayer money going to universities was cut dramatically in 2012, so that the majority of the taxpayer contribution now comes through subsidizing income contingent loans. Thus calculating taxpayer funding requires simulating both interest rates and graduates’ projected earnings, because the income-contingent loan system subsidizes interest for low-earning graduates and includes loan forgiveness for those with persistently low earnings. If anything, however, recent estimates of taxpayer liability may be substantially overstated as the actual cost of government borrowing has been lower than anticipated, and college graduates continue to earn high returns in the labor market even as the number of graduates has expanded. [18]

Universities benefited from the increased resources, but so did students themselves: a key consequence of the reforms was to enable students to access more of their future earnings to support current expenses while enrolled. (Not captured by this table is the redistribution that occurred within the population of graduates: by design, low-earning graduates pay back less of their borrowed funds than do high-earners.)

Table 2. Total annual funding flows

| 1997-98 | 2003-04 | 2008-09 | 2011-12 | 2012-13 | |

| Funding sources: | |||||

| Taxpayers | 3.5 | 5.6 | 6.7 | 6.4 | 5.9 |

| Graduates | 0.2 | 0.6 | 1.1 | 5.2 | 7.9 |

| Funding recipients: | |||||

| Universities | 3.1 | 5.5 | 6.7 | 6.2 | 7.8 |

| Students | 0.7 | 0.5 | 1.1 | 5.4 | 6.0 |

| Sources: Authors’ calculations using estimates from Belfield et al. (2017), Dearden et al. (2008), and Chowdry et al. (2012, erratum). See endnotes for additional details. [19] | |||||

What happened with quality, enrollment, and equity in the post-reform era?

Rigorously assessing the causal impacts of the 1998 and subsequent reforms is not straightforward due to the widespread, drawn out, and multifaceted nature of the changes. The available causal evidence does suggest that students in England are responsive to prices, holding all else constant, just as they are in the U.S. [20] But a critical aspect of the argument for introducing fees was that all else would not be held constant. Our goal here is to take a step back to examine the broad arc of the new system’s consequences over time: Did quality increase? Did enrollments expand? Did socioeconomic gaps in enrollment narrow? We examine each question in turn.

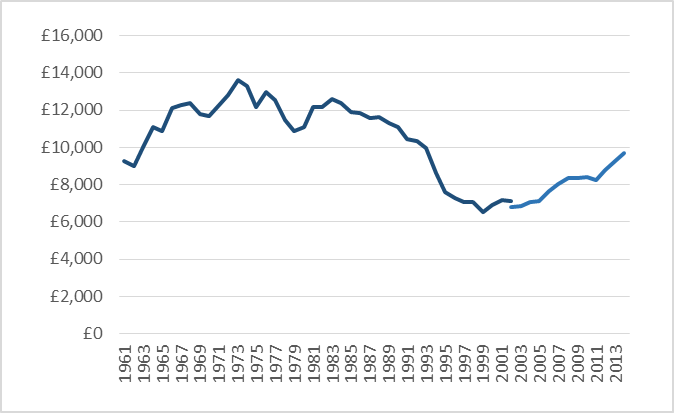

• Did the quality of university education increase in the years following the 1998 overhaul?

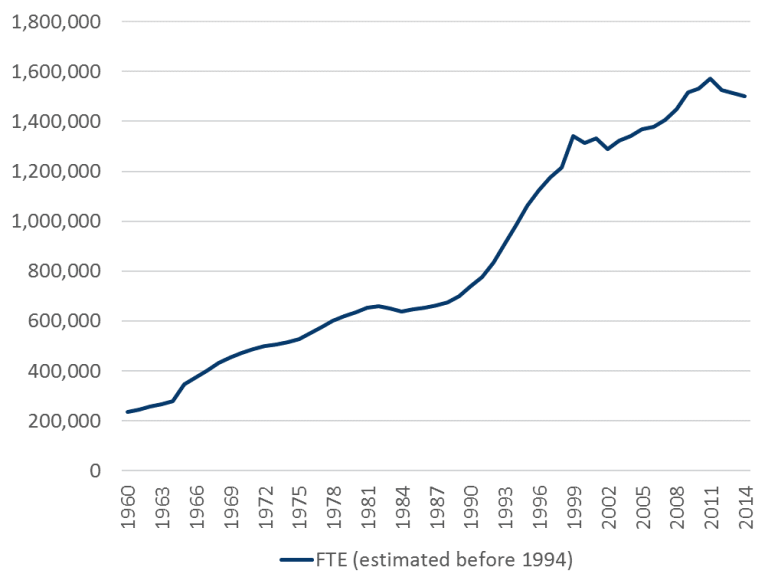

Yes: perhaps the most obvious impact of the 1998 reform has been a clear reversal of the trends in per-student institutional resources. We do not have any data on concrete measures of quality, such as class sizes or reliance on non-tenure-track faculty. [21] Still, how much institutions spend to educate each student can serve as a rough proxy for institutional quality. And Figure 5 shows that resources per full-time equivalent student (including both government funding and tuition revenue) has increased by nearly 50 percent since reaching a historical low in 1999 (just after the reform, when most students were still grandfathered under the old system).

Figure 4. Average funding per full-time equivalent student

Sources: Carpentier (2004) and authors’ calculations. [22]

• Did enrollment increase in the years following the 1998 overhaul?

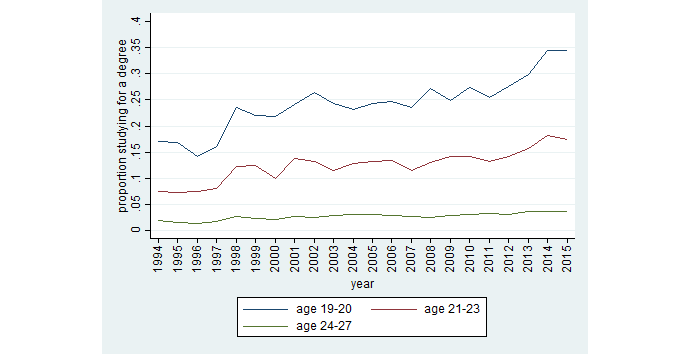

Yes: Figure 5, which uses administrative data to track enrollments before and after the 1998 reform, shows that aggregate enrollments continued to rise if at a somewhat slower rate. But these data include foreign students and some others not subject to the fee policies and do not account for changes in cohort size. Thus, we draw upon data from the national Quarterly Labor Force survey in Figure 6 to examine changes in enrollment rates for English nationals. [23]

Figure 5. Full-time equivalent undergraduate enrollments over time

Source: Authors’ calculations using publicly available data from the Higher Education Statistical Agency (HESA). [24]

Figure 6 indicates that enrollment rates have more than doubled among traditionally-aged students since the 1998 overhaul, from around 16 percent in the years just prior to the change to around 35 percent in 2015. About half of this increase occurred right around 1998, possibly as a result of relaxed quotas negotiated as part of the initial reform package. Enrollment rates among older age groups have also approximately doubled. If anything, the increases appear to accelerate after the major changes of 2012.

Figure 6. University enrollment rates by age group over time

Source: Wyness calculations using restricted-access data from Secure Lab: SN6727 Quarterly Labour Force Survey, 1992-2016: Secure Access.

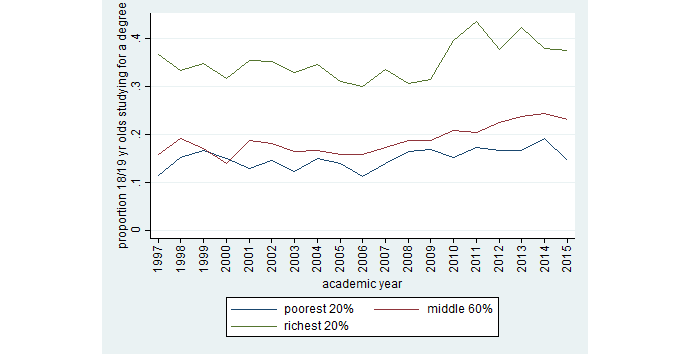

• Have socioeconomic gaps in enrollment declined after the 1998 reforms?

They have at least stabilized. We can use the same Quarterly Labor Force survey data to examine enrollment rates by parental income, for young students who are still classified as part of their parents’ household. Figure 7 below shows that while enrollment is higher now for all groups than it was in 1997, the gap between income groups remains large. This pattern is consistent with evidence from longitudinal cohort studies at least up through 2005. Blanden & Machin (2013), who documented the rising income gap in college attainment during the 1980s and 1990s, found that the gap shrunk slightly in the years just after the reform (from 37 percentage points in 1999 to 34 percentage points in 2005). [25]

Figure 7. Percentage of 18/19 year-olds enrolled in college, by parental income

Source: Wyness’ calculations using Secure Lab: SN6727 Quarterly Labour Force Survey, 1992-2016: Secure Access data. Figure cannot be extended prior to 1997 due to small sample sizes.

Our own analysis of administrative enrollment data, which allows us to examine family background for all students (not just the youngest ones) and for years including the most recent policy changes, tells a somewhat more optimistic story. Between 2002 and 2014, students from low-SES (or in English terminology, low-SEC) backgrounds grew from 28 percent to 33 percent of all enrollment.

Discussion and implications for the “free college” debate in the U.S.

Putting all of the evidence together, has the new English system lived up to its progressive goals? Although it is difficult to know what would have happened in the absence of reform, the trends appear to be moving in the right direction. Per-student educational resources increased substantially, after years of steady decline, while enrollments continued on an upward trajectory. Income and socioeconomic gaps, which had widened dramatically in the 1980s and 1990s, also appear to have stabilized or slightly declined.

Given that tuition prices went from zero to £9,250, and given that English graduates now hold substantially greater debt on average than U.S. graduates, the pattern of consequences described above is rather remarkable. The system has certainly not imploded in the way critics may have feared.

So what implications does the English experience hold for the U.S. debate about free college?

First, policymakers should shift away from focusing solely on net prices to also thinking about net liquidity: the costs students face and the resources they have access to up-front. A critical feature of tuition fees in the English system is that no student has to pay anything up front: the full amount can be financed via government loans (in other words, fees are effectively deferred until after graduation). Thus, while college is no longer free in England, it remains free at the point of entry. And even though tuition has risen, students have access to more resources than ever before to help pay for all the other costs that might stand in the way of enrollment (e.g., housing, food, books, and transportation).

Second, the income-contingent loan (ICL) repayment system put into place in 1998 is what makes it possible for students to safely borrow much higher amounts than they could in the U.S. system. Monthly repayments are calculated as a fraction of income earned above a minimum level (currently, 9 percent of income above £21,000) and collected via the payroll tax system, so payments are manageable in size, the administrative burden is low, and the risk of default is minimized. In the U.S., student loan limits are too low to cover even tuition at the typical public four-year institution, let alone the non-tuition costs of attendance, and many students default on debts well below the maximum levels. For a detailed description of the English ICL system and its lessons for the design of U.S. student loans, see Barr, Chapman, Dearden, and Dynarski (2017). [26]

Finally, the English experience leading up to the 1998 reforms starkly illustrates the key challenge of a free university system: insufficient resources. Lack of funding can lead to declining quality, caps on quantity, or both, and prioritizing free tuition for all means less money to help the neediest students with additional costs. These risks are not hypothetical in New York’s new plan: they are already foreshadowed in its fine print. The New York legislation stipulates that if the costs outstrip available funds, awards may be rationed by lottery or by adding additional criteria (the plan already includes stringent GPA, credit-completion, and post-college residency requirements). No additional funds are promised to institutions, raising the likelihood that per-student resources will fall as enrollments increase. And no additional funds are promised for low-income students, whose tuition is often already fully covered by existing grants, but who may struggle to pay for rent, food, books, and gas.

None of this is meant to argue that the English system is perfect. While the loan repayment structure facing graduates is much more progressive than in the past, we show above that the structure of pricing and financial assistance by family income is not any more progressive than it was before the reforms (though students from all income backgrounds have more liquidity). This may help explain why gaps in access and attainment have not shrunk more substantially over time.

Since 2006, English institutions have been required to direct at least 10 percent of tuition revenues towards means-tested institutional grants (bursaries), a feature not reflected in our figures. Yet it is highly unlikely that students know about this institution-level aid when they are making their enrollment decisions since there is no easy way for students to obtain this information. [27] Moreover, since 2015, centralized maintenance grants have been abolished, with loans extended to make up the difference, meaning that although their liquidity is unaffected, students from poorer backgrounds now graduate with more debt than those from richer backgrounds. Reducing the college attainment gap further may depend upon introducing greater progressivity into the centralized schedule of fees, grants, and loans, as well as upon efforts to reduce the disparities in pre-college qualifications by parental background.

Rather than looking to emulate the English model of the 1990s, the U.S. might instead consider emulating some key features of the modern English system that have helped moderate the impact of rising tuition, such as deferring all tuition fees until after graduation, increasing students’ ability to cover living expenses, and automatically enrolling all graduates in an income-contingent loan repayment system that minimizes both paperwork hassle and the risk of default. No model is without its challenges. But the English experience suggests that making college completely free is hardly the only path to increasing quantity, quality, and equity in higher education. Indeed, the story we tell here shows how a free system can sometimes work against these goals.

— Richard J. Murphy, Judith Scott-Clayton and Gillian Wyness

Richard J. Murphy is an Assistant Professor at the University of Texas at Austin Department of Economics. Judith Scott-Clayton is Associate Professor of Economics and Education at Teachers College, Columbia University. Gillian Wyness is Senior Lecturer in Economics of Education at the University College London Institute of Education.

Richard J. Murphy is an Assistant Professor at the University of Texas at Austin Department of Economics. Judith Scott-Clayton is Associate Professor of Economics and Education at Teachers College, Columbia University. Gillian Wyness is Senior Lecturer in Economics of Education at the University College London Institute of Education.

This post originally appeared as part of Evidence Speaks, a weekly series of reports and notes by a standing panel of researchers under the editorship of Russ Whitehurst.

The author(s) were not paid by any entity outside of Brookings to write this particular article and did not receive financial support from or serve in a leadership position with any entity whose political or financial interests could be affected by this article.

Notes:

1. Students still have to pay mandatory fees ranging from 10 to 25 percent of the tuition bill, and still have to cover textbooks and other necessary supplies. Part time students are completely excluded, as are many full-time students (students must complete at least 30 credits per year to renew, more than the 24 credits required for full-time status), and students must live in-state for a specified period after leaving school or else the scholarship is converted to a loan.

2. UK maximum tuition charges are for the 2017-18 academic year. See https://www.ucas.com/ucas/undergraduate/finance-and-support/undergraduate-tuition-fees-and-student-loans.

3. English students can borrow for living expenses in addition to the cost of tuition. Average debt figures for England are from Philip Kirby (2016), Degrees of Debt, London, England: The Sutton Trust. URL: http://www.suttontrust.com/newsarchive/english-students-face-highest-graduate-debts-exceeding-ivy-league-average/. Average debt in the U.S. for BA graduates with debt is $24,842 and excludes 34% that did not borrow at all (authors’ calculations using Quick Stats with Baccalaureate & Beyond 2008 data).

4. The reforms we describe below also apply to Northern Ireland. However, enrollment in Northern Ireland is very small relative to enrollment in England (less than 3 percent of combined enrollment). In addition, because students from Northern Ireland hold Irish passports, they can still take advantage of tuition-free public institutions outside of England. For these reasons we focus our analysis on the English experience.

5. While the English system includes a handful of private institutions, nearly all university enrollment takes place via the public system. Even during this “free college” era there was a concept of tuition fees, but they were paid by local education agencies directly to the national government and largely invisible to students (Dolton, P. & Lin, L. (2011), ‘From grants to loans and fees: the demand for post-compulsory education in England and Wales from 1955 to 2008’, CEE Discussion Paper No. CEEDP0127, Centre for Economics of Education, London School of Economics). Finally, note that while the U.S. vocabulary draws a distinction between “tuition” and “fees,” the common UK term is simply “fees.” In this report we use the terms tuition, fees, and tuition fees interchangeably.

6. All currency amounts are converted to 2015 equivalents. Wyness calculations using data from Carpentier, V. (2004). Historical Statistics on the Funding and Development of the UK University System, 1920-2002. [data collection]. UK Data Service. SN: 4971, http://doi.org/10.5255/UKDA-SN-4971-1.

7. For comparison, the high-low income gap in BA/BS attainment in the U.S. went from 31 to 45 percentage points over a similar time period (Bailey and Dynarski, 2011). Interestingly, attainment rates for low-income students are quite similar between the U.S. and UK over this time period (growing from about 5 percent to about 10 percent in both countries). Attainment rates for high-income students were higher in both periods for the U.S., but rose faster in the UK.

8. Note that because of the highly structured, three-year university curriculum in England, persistence and completion rates are very high among those who enroll. See Crawford, C. (2017), ‘Socio-economic differences in university outcomes in the UK: drop-out, degree completion and degree class,’ IFS Working Paper W14/31, Institute for Fiscal Studies, London; Murphy, R. & Wyness, G. (2015), ‘Testing Means-Tested Aid’, CEP Discussion Paper No’ CEPDP1396, Centre for Economic Performance, London School of Economics.

9. The statistics underlying this figure are from Blanden, J. and Machin, S. (2013) Educational Inequality and The Expansion of United Kingdom Higher Education, Scottish Journal of Political Economy, 60, 597-598. Note: the cohort turning 23 in 1999 was minimally affected by the 1998 reforms, as most of English students graduate by age 22.

10. Although in the U.S., tuition and fees have slightly different meanings, here we use the terms tuition, fees, tuition fees, and top-up fees interchangeably.

11. Dearing, R. (1997), ‘Higher Education in the learning society, Report of the National Committee of Enquiry into Higher Education, HMSO, London.

12. For an excellent overview of how the English ICL system and how it compares with the U.S. student loan system, see Nicholas Barr, Bruce Chapman, Lorraine Dearden, and Susan Dynarski, “Getting student financing right in the U.S.: lessons from Australia and England,” Centre for Global Higher Education Working Paper No. 16 (March 2017), London, England: Centre for Global Higher Education. http://www.researchcghe.org/perch/resources/publications/wp16.pdf.

13. See Barr, N.A. & Crawford, I. (1998). The Dearing Report and the government’s response: a critique’ London: LSE Reasearch Online, http://eprints.lse.ac.uk/archive/0000283. Also see Barr, N.A. (2010), ‘Paying for higher education: What policies, in what order?’ Submission to the Independent Review of Higher Education Funding and Student Finance, http://econ.lse.ac.uk/staff/nb/Barr_HEReview100215.pdf.

14. Information assembled from Student Loans Company, 2012 “Student Loans: A Guide to Terms & Conditions – Student Finance England (PDF 210kB)” (PDF). Student Loans Company. Retrieved 15 March 2017; also from Smith, M. “Timeline: tuition fees,” The Guardian, January 27, 2004, https://www.theguardian.com/education/2004/jan/27/tuitionfees.students. Note that amounts in this table are in current-year pounds sterling. All figures for tuition fees, grants and loans are per year (with the typical UK degree taking 3 years).

15. Maintenance loans, in English vocabulary, refer to the loans students can obtain to cover living expenses. Fee loans cover the tuition fee so that students do not have to pay any fees upfront. An alternative way to define net liquidity, which would result in the same number, would be: grants plus maintenance loans plus fee loans, minus all fees.

16. Note, that these charts do not include institutional need-based grants, referred to as “bursaries” in the English system, which institutions were expected to expand using their new tuition revenues, nor do they reflect changes in loan repayments among graduates, which have clearly become more progressive under the ICL system. It is also worth noting that 2012 changes to the ICL repayment schedule resulted in increased progressivity at least from graduates’ point of view because of the increase in the repayment threshold to £21,000, and the introduction of real interest rates (the latter disproportionately affect higher income graduates who are more likely to repay their loans in full).

17. See Student Loans Company, 1991-2015, Student Support for Higher Education in England.

18. In fact, a recent analysis from the IFS shows that the figure for taxpayer expenditure on HE in 2012 may be significantly over-estimated. This is mostly because the government’s cost of borrowing (i.e. discount rate) at the time of the 2012-13 analysis was assumed to be 2.2 percent. However, more recent analysis by the government shows that cost of borrowing was far lower—at 0.7 percent (Belfield, C., C. Crawford & L. Sibieta (2017), Long-run comparisons of spending per pupil across different stages of education, IFS Report R126, Institute for Fiscal Studies, London). Hence the cost to the taxpayer of subsidizing loans may be considerably lower than was originally assumed. Moreover, the returns to degree attainment appear to have held strong even as higher education expanded dramatically (see Ian Walker and Yu Zhu (2013), ‘The Impact of University Degrees on the Lifecycle of Earnings: some further analysis’, BIS Research Paper No.112, Department for Business, Innovation and Skills, London).

19. The 1997-98 figures are based upon Belfield, C., C. Crawford & L. Sibieta (2017), Long-run comparisons of spending per pupil across different stages of education, IFS Report R126, Institute for Fiscal Studies, London. The 2003-04 through 2001-12 figures are from Dearden, L., Fitzsimons, E., & Wyness, G. (2014), “Money for nothing: estimating the impact of student aid on participation in Higher Education” Economics of Education Review, Volume 43, December 2014, 66–78. The 2012-13 amounts are based upon Chowdry, H., Dearden, L., Goodman, A., & Jin, W. (2012, erratum). The distributional impact of the 2012–13 higher education funding reforms in England. Fiscal Studies, 33(2), 211-236. Chowdry et al. report per-student figures; we convert to aggregate amounts using their estimated cohort size of 307,000. Taxpayer expenditures may be overestimated in 2012-13 due to lower than expected interest rates; see previous note.

20. Dearden, Fitzsimons & Wyness (2014) look at the effect of reinstating means-tested grants in 2004, using a difference-in-difference strategy that compares enrollment before and after the 2004 reinstatement (during a period when tuition fees and loan limits were stable), for students from low- and high-income families. They estimate a positive effect on enrollment rates for low-income 18-19 year-olds, on the order of 4 percentage points for a £1,000 grant. A working paper by Sá (2014) examines the effect of the dramatic fee increase in 2012, comparing enrollments in England to those in Scotland (which was unaffected) before and after the change. Sá estimates a large (33 log points, or 40 percent) reduction in attendance among white students in England after this change, with much smaller effects for other race/ethnicities. The magnitude of this estimated effect is difficult to square with observed enrollment trends (which did decline noticeably, but hardly by 40 percent). The estimate could be affected by functional form misspecification (the difference-in-difference strategy is not invariant to functional form decisions such as whether to measure trends in levels or logs), or by a violation of the assumption that England and Scotland would follow similar paths absent the change. See Deming and Dynarski (2012) for a review of the U.S. literature.

21. In the U.S. context, it would also be natural to look at trends in completion rates conditional on enrollment. In the UK, however, course curricula are highly structured and nearly all university entrants complete. See Crawford, C. (2017), ‘Socio-economic differences in university outcomes in the UK: drop-out, degree completion and degree class’, IFS Working Paper W14/31, Institute for Fiscal Studies, London; Murphy, R. & Wyness, G. (2015), ‘Testing Means-Tested Aid’, CEP Discussion Paper No’ CEPDP1396, Centre for Economic Performance, London School of Economics.

22. Statistics for 1955-2002 are taken from Carpentier, V. (2004), Historical Statistics on the Funding and Development of the UK University System, 1920-2002 [data collection], SN: 4971, http://doi.org/10.5255/UKDA-SN-4971-1, London: UK Data Service. Statistics for 2002-2014 are calculated by Gillian Wyness using the Higher Education Information Database for Institutions (HEIDI), 2000-2014, London: The Higher Education Statistics Agency Limited. All figures expressed in constant 2015 pounds sterling. FTE enrollments used in the computation contain all student types (full-time, part-time, postgraduate, undergraduate, UK, EU, overseas); funding per head is for all students and comprises teaching grants and tuition fees.

23. Unfortunately, due to data limitations, we cannot extend this series prior to 1994.

24. HESA (2002-2015) ‘UK Performance Tables’ Published by Higher Education Statistical Agency, https://www.hesa.ac.uk/data-and-analysis/performance-indicators/summary. The underlying HESA data exclude enrollment in polytechnics prior to 1994. We estimate total enrollment for earlier years assuming that both types of institutions grew at the same rate in the year of the change, and that enrollment at these institutions was a constant fraction of total enrollment.

25. Blanden, J. and Machin, S. (2013) Educational Inequality and The Expansion of United Kingdom Higher Education, Scottish Journal of Political Economy, 60, 597-598.

26. Barr, N.A., Chapman, B., Dearden L., Dynarski, S. (2017) ‘Getting student financing right in the U.S.: lessons from Australia and England’ Centre for Global Higher Education, March 2017, http://www.researchcghe.org/publications/getting-student-financing-right-in-the-us-lessons-from-australia-and-england/.

27. Murphy, R. & Wyness, G. (2015), ‘Testing Means-Tested Aid’, CEP Discussion Paper No’ CEPDP1396, Centre for Economic Performance, London School of Economics.