For many teachers, a defined-benefit pension plan at retirement is hardly a “fringe” benefit—rather, it is a long-anticipated payoff at career’s end, after years of modest take-home pay. Public school teachers who stay on the job for 25 or 30 years count on retiring in relative security, with monthly benefit payments until death.

But for many young teachers, that pension promise is broken. Nationwide, teachers’ plans are drowning in $500 billion in debt, driven in part by a financial crisis in which nearly all state plans failed to meet their target rates of return. To balance the books, states are requiring increased employee contributions and are making vesting rules more stringent—using new teachers’ paychecks to protect legacy payments to older colleagues. As a result, month after month, many teachers turn over a substantial portion of their pay to a plan whose benefits they are unlikely to receive.

While these changes may improve the short-term financial health of teachers’ pension plans, their long-term viability looks bleak without more significant structural reforms. This will prove a challenge for public school districts, most of which are required by law to participate in their state’s plan.

In some states, however, public charter schools provide an important alternative: charters have the flexibility to opt out of the state pension plan and develop their own retirement plans. The charter sectors in these states have the opportunity to serve as laboratories of innovation, not only in terms of educational programs but also as examples of management strategies that could be applied to the broader teacher labor market.

To explore this possibility, we studied retirement plans and surveyed charter schools in five states with such flexibility: Arizona, California, Florida, Louisiana, and Michigan. We find a growing number of schools, especially those run by management organizations, are choosing to opt out of state pension plans. In lieu of standard plans, charters are providing various, more portable defined-contribution options and incentives such as 401(k) and 403(b) plans, potentially providing a new way to ensure that teachers’ retirements are secure. In interviews, charter operators detail their reasons for these choices, providing important context to a retirement challenge that is unlikely to be resolved without significant action.

A Growing Pension Problem

Keeping public-school teachers’ pensions plans flush is expensive, and it accounts for a growing share of education spending.

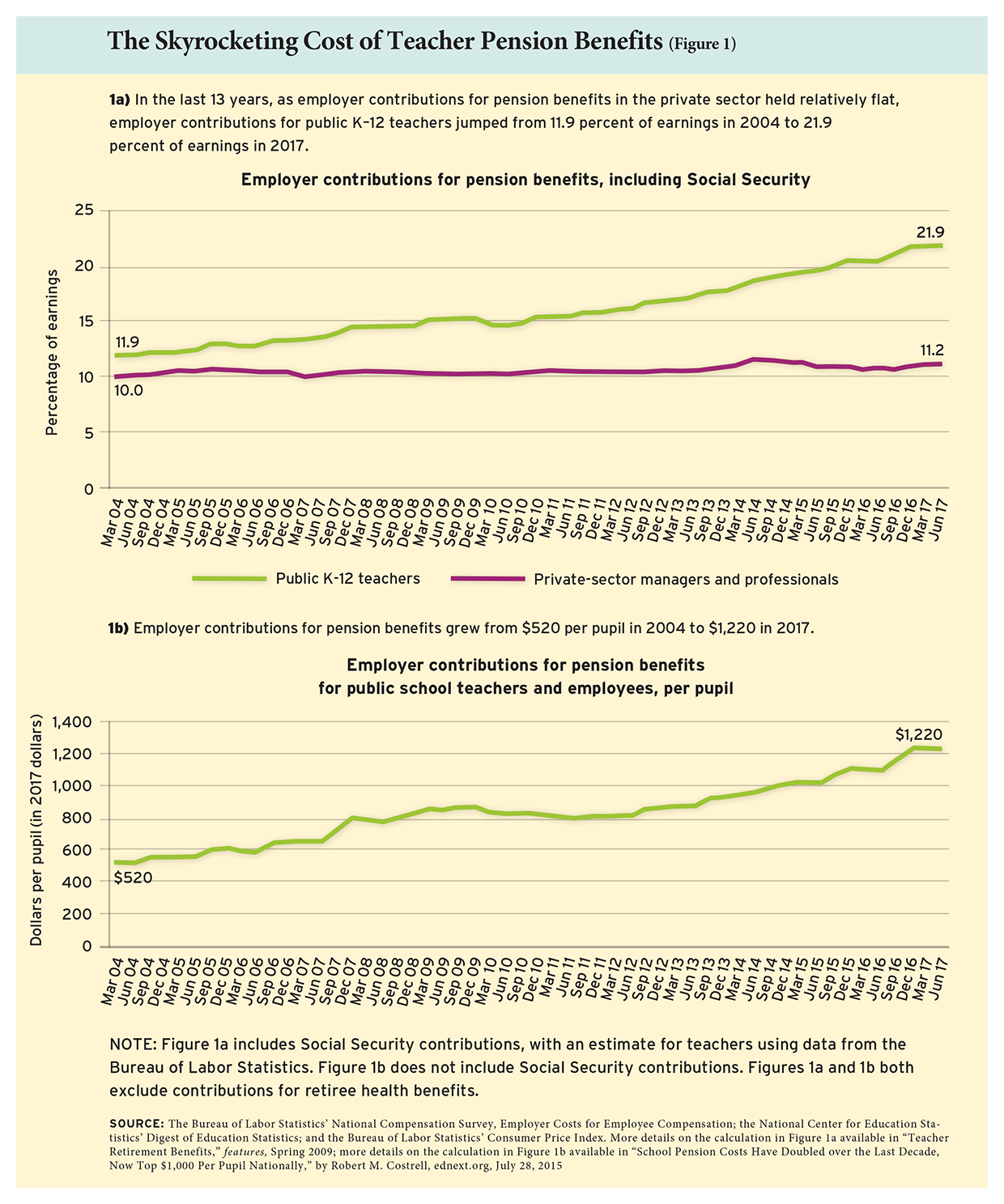

In 2017, employer costs for teacher retirement benefits accounted for 21.9 percent of teachers’ salary costs, up from 11.9 percent in 2004 (see Figure 1). By contrast, in the private sector, retirement benefit costs for workers account for roughly 11 percent of salaries, a share that has remained relatively flat over the same time period. Pension costs, excluding Social Security and retiree health insurance, have grown from $520 per student in 2004 to $1,220 today in current dollars—or from roughly 5 percent to 10 percent of current expenditures per student.

Since the start of the financial crisis in 2007, 32 states have increased employee contribution rates and 37 states have increased employer contribution rates. States like California have publicly stated that these contribution rates will continue to increase in the future. In other states, like Illinois and Michigan, future increases to employee and employer contributions rates seem like a near certainty given the poor fiscal health of their plans.

At the same time, many states have reduced benefits for new teachers. Between 2007 and 2015, nine states passed laws that increased the vesting period for new teachers from 5 years to 10 years on the job. In addition, 29 states tightened retirement eligibility rules by increasing the retirement age, required years of employment, or both.

This is problematic because, unlike in most professions, teachers’ pension plans are not portable across states—and, in some cases, even within states (see “Golden Handcuffs,” research, Winter 2010). For example, a teacher who moves from New Jersey to New York has to change plans and cannot continue to accrue benefits. If she moves before she is vested in the New Jersey plan, she may only withdraw her contributions and loses out on any pension benefits. This severe penalty is widespread: in most states, fewer than half of new teachers are expected to stay long enough to receive any pension benefits at all (see “Why Most Teachers Get a Bad Deal on Pensions” at www.educationnext.org). In Washington, D.C., and 10 states—Arizona, Colorado, Maine, Mississippi, Nebraska, New Hampshire, South Dakota, Texas, Vermont, and Wyoming—fewer than 10 percent of new teachers are expected to remain in the state system long enough to be eligible for normal retirement benefits. Yet state pension plans remain a central part of teachers’ pay packages, especially since 40 percent nationwide do not participate in Social Security.

Data

One group of public school teachers is not automatically locked into these pension programs: teachers working in charter schools. In 19 states, charters may choose to participate in their state’s pension plan, or may offer teachers an alternative.

Arizona, California, Florida, Louisiana, and Michigan have large numbers of charter schools and allow for flexibility regarding state plan participation. All five states provide traditional final average salary defined-benefit plans to teachers, with some differences. Florida allows all teachers to opt into an alternative defined-contribution plan. In Arizona, Florida, and Michigan, teachers participate in Social Security. In California and Louisiana, teachers in district schools do not participate in Social Security, but teachers who work in a charter school that has opted out of the state pension plan must do so.

To gather details on the schools, we use two years of data from the National Alliance for Public Charter Schools: 2014-15 for Arizona and Michigan, and 2015-16 for California, Florida, and Louisiana. The organization maintains a comprehensive database of every charter school’s management type, year opened, grades served, and geographic location, among other variables, collected from state education departments and the U.S. Department of Education’s Common Core of Data. We also reviewed individual state pension-plan information, in the form of either a list of schools that participated or annual financial audits that list the members of the plan. In Louisiana, plan participation data were provided by the charter support organization, the Louisiana Association of Public Charter Schools.

Which Charters Opt In?

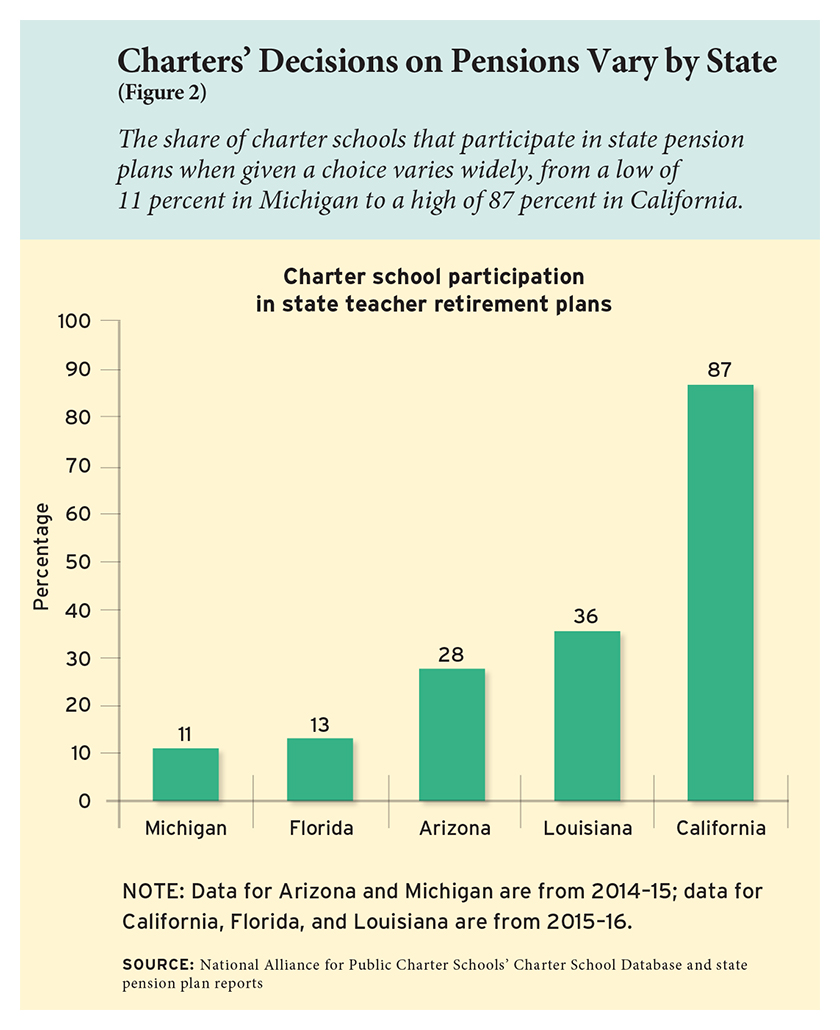

Across the five states that we studied, 47 percent of charter schools participated in their state’s pension plan. However, the rate varied considerably from state to state, from a low of 11 percent in Michigan to a high of 87 percent in California (see Figure 2).

Across the five states that we studied, 47 percent of charter schools participated in their state’s pension plan. However, the rate varied considerably from state to state, from a low of 11 percent in Michigan to a high of 87 percent in California (see Figure 2).

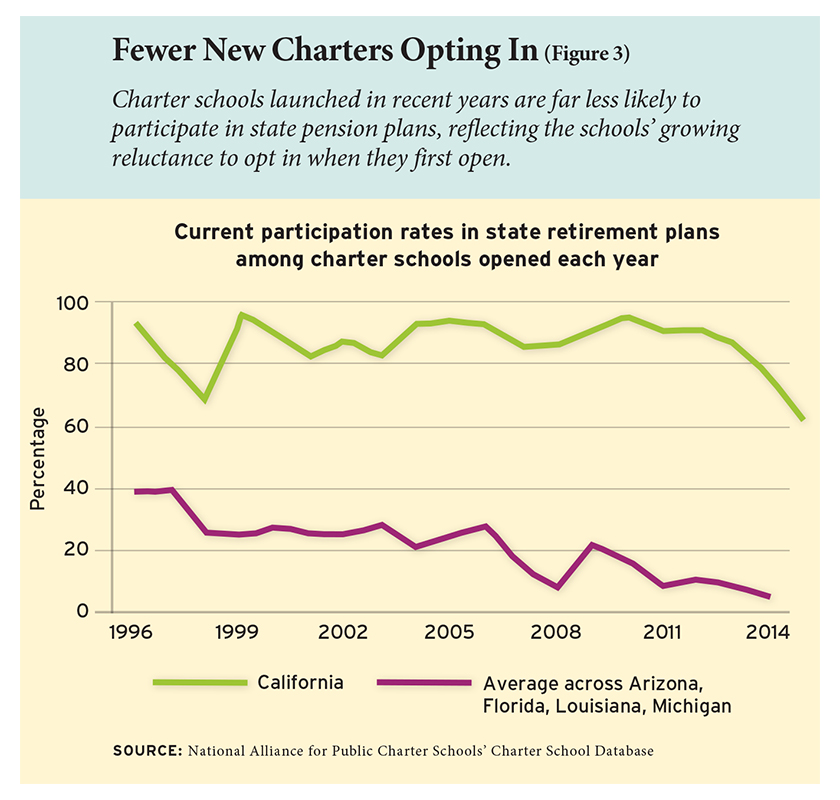

In Figure 3, we plot the charter participation rate against the year in which the charter opened. Because it is very difficult for a charter school to opt out of a state plan once it has enrolled teachers, whether a school is currently participating generally reflects a decision it made before it opened its doors. Once doors are open and teachers are hired, the in-or-out status is largely fixed. It is therefore notable that we find a clear downward trend from about 2010 on, when pension costs began to rise sharply, with newer charter schools much less likely to participate in the state plan.

Since California has as many charter schools as the other states combined, as well as much higher participation rates, we plot its trend separately. The share of new charter schools opting into the state plan hovered around 90 percent until 2013—the tail end of the Great Recession. Since then, the participation rate of new schools has dropped precipitously, reaching a new low of 63 percent in 2015‒16. The downward trend began when a new state law intended to shore up ailing plans set dramatic increases in contribution rates. Districts’ and charter schools’ contributions were set to more than double in seven years, from 8.25 percent to 19.1 percent of payroll by 2020; currently, they are at 14.4 percent. Teacher contributions grew as well, from 8 percent of salary to 10.25 percent.

However, of the five states in our study, only California also provides a direct payment from the state legislature to subsidize the cost of the pension plan. Currently, the state contributes 8.8 percent of payroll toward teacher pension costs. In the past, this subsidy seemed to incentivize charter schools to stay in the state plan; however, rising employer contributions have undoubtedly changed that calculation moving forward.

However, of the five states in our study, only California also provides a direct payment from the state legislature to subsidize the cost of the pension plan. Currently, the state contributes 8.8 percent of payroll toward teacher pension costs. In the past, this subsidy seemed to incentivize charter schools to stay in the state plan; however, rising employer contributions have undoubtedly changed that calculation moving forward.

Differences by School Type

In order to better understand some of the factors that influence charter participation, we estimate a statistical model relating charter school participation to characteristics of the charter school, the market in which the school operates, and a time trend. We look at single-site, independent charter schools, and schools that are part of two different kinds of networks: nonprofit charter-management organizations (CMOs) and for-profit education-management organizations (EMOs).

Our model indicates that schools that are part of CMOs and EMOs are considerably less likely to participate in state plans compared to single-site charters. EMOs seem particularly averse to participation in costly defined-benefit plans, and participate at one-quarter the rate of similarly situated independent charter schools. For example, if 60 percent of independent charter schools participated in the pension plan in a particular state, then we would expect that only 15 percent of EMOs would participate.

Both nonprofit and for-profit management organizations appear more likely to opt out and offer individual defined-contribution plans for employees, such as 401(k) plans (or for nonprofits, similar but lower-cost 403(b) plans). CMOs and EMOs may be better positioned to absorb the fixed costs associated with setting up an alternative retirement plan, can more easily assemble the required expertise, and often operate in more than one state, and thus would likely favor mobile benefits that facilitate staff moving from one school to another.

In Arizona, Florida, Louisiana, and Michigan, we also find differences among school types: charter middle schools and particularly high schools are more likely to participate in state plans than are charter elementary schools. Middle schools and high schools are 21 percent and 91 percent, respectively, more likely to participate in state plans. Survey data routinely show that the public elementary schools have an easier time filling teaching vacancies compared to their middle-school and high-school peers. It is thus not surprising that elementary-level charter schools would be more likely to find that the costs of pension participation exceed any potential benefits in recruitment and retention, since they find it easier to fill their teaching vacancies.

Geographic surroundings matter, too. Charter schools operating in urban and suburban areas are considerably less likely to paticipate in state plans than rural charter schools, although the gap is not statistically significant in California. One interpretation is that charter schools operating in more populated urban and suburban markets may find it easier to fill vacancies with teachers who do not have previous public-school experience. They may also find it easier to tap alternative sources of teachers like local teacher residency programs, Teach for America (TFA), or other college graduates who are less inclined to spend a full career in teaching. Charters in rural environments may have a smaller pool

of such candidates, forcing them to more aggressively recruit teachers from district schools and to offer a retirement

benefit package that is comparable in order to recruit qualified candidates.

Charters Explain Their Pension Choices

To better understand why charter schools choose to opt in or out of pension plans, we administered surveys to a random sample of schools across the five states. By design, half of the schools in our sample participated in their state’s pension plan and half opted out. Our overall response rate was 22 percent; on the whole, respondents resembled non-respondents. Roughly 100 schools are included in our analysis. In addition, for the subsample of schools that indicated a willingness to do so, we also followed up with a phone interview.

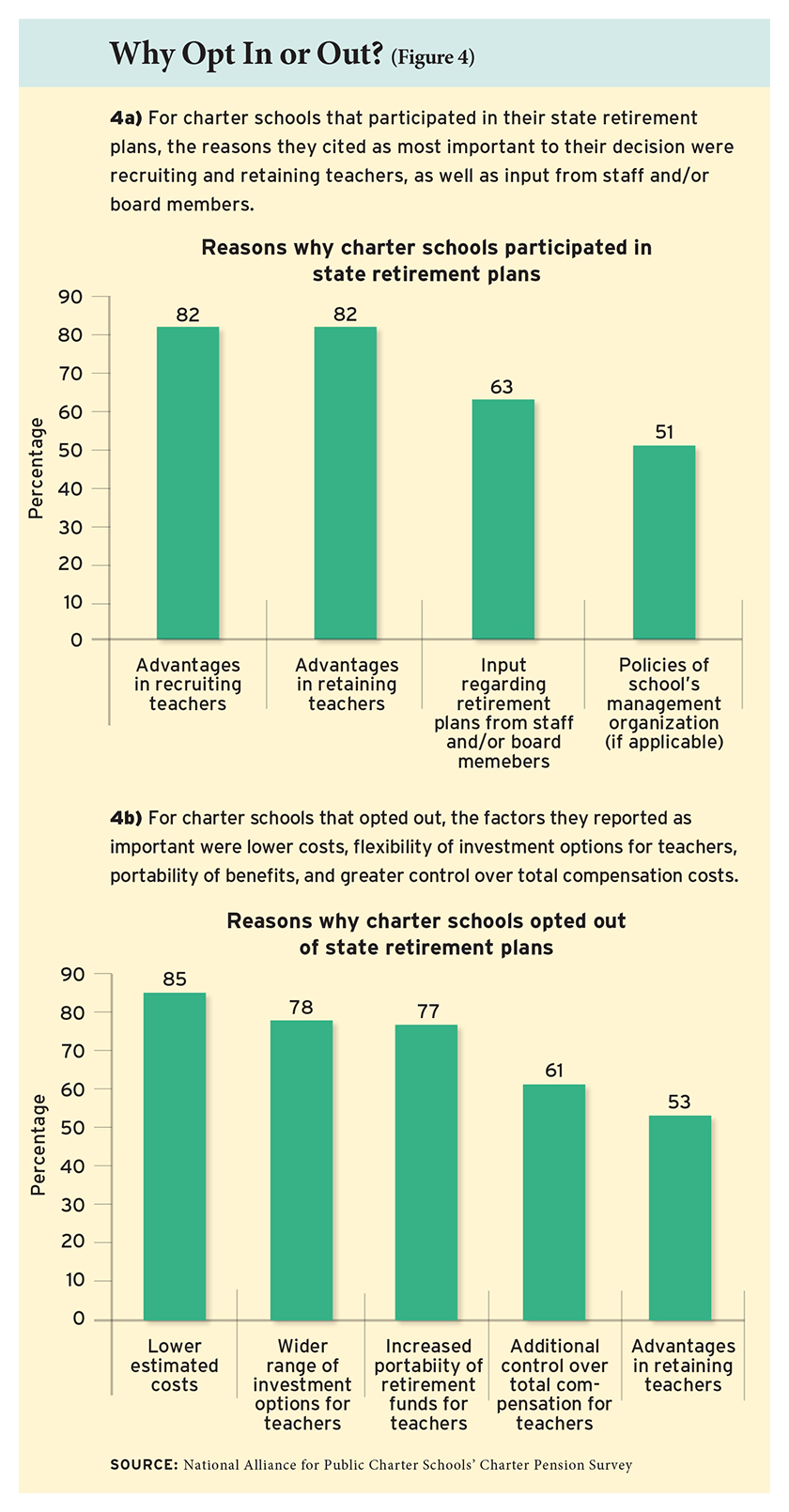

We find that, for charter schools that participated in the state plan, the primary reasons were recruiting and retaining teachers, as well as input from staff and/or board members (see Figure 4). As one charter school administrator put it:

We find that, for charter schools that participated in the state plan, the primary reasons were recruiting and retaining teachers, as well as input from staff and/or board members (see Figure 4). As one charter school administrator put it:

In the State of California, participating in the State Teachers’ Retirement System is an expectation for teachers. They actually anticipate their participation in the retirement system. If we did not participate, we would impact our ability to recruit highly effective, quality teachers.

However, for charter schools that opted out, the primary drivers were lower costs, flexibility of investment options for teachers, portability of benefits, and greater control over total compensation costs. Below are two examples from phone interviews with two different school administrators:

Our 401(k) matching structure incentivizes staff to continue working for us by increasing our match over time. However, we also immediately vest employees so that they have the security of a fully portable plan; they can take their contributions, our matching dollars, and all the earnings when/if they leave our employ. We have found that many high-quality teachers don’t necessarily have the next 20 years planned out. Giving them a retirement benefit that is much more flexible than the state’s pension plan is very attractive to them.

Opting out of the state pension plan frees up about $1 million at each school. We then have the freedom to use that $1 million in ways that our employees most value and that ultimately drive student achievement. We’re able to direct our personnel budget to the items that staff most value, like higher salaries, matching contributions on a portable 401(k) plan, offering flexible spending accounts, and setting up discounted quality childcare. It also frees up money for classroom items, computer labs, afterschool sports, and field trips.

Alternative Retirement Plans

When charter schools opt out of state plans, what, if anything, do they put in its place? The vast majority offer their teachers an alternative—mainly portable, defined-contribution plans. Some 68 percent offer a 401(k) and 25 percent offer a 403(b) plan (a similar, but lower-cost option for tax-exempt organizations). In states like California and Louisiana, where district teachers do not participate in Social Security, charter teachers not in the state pension plan also receive Social Security coverage.

One dramatic difference between charter and traditional plans concerns vesting periods, or the amount of time a teacher must spend at her job before she becomes eligible for full pension benefits. In traditional state pension plans, it often takes at least 5 years for new teachers to become vested, and 15 states currently require 10 years to vest. As a result, many short-term or mobile teachers will fail to become vested and will not receive the full benefits matched to the contributions they made. By contrast, alternative retirement savings plans for charter teachers have much shorter vesting periods: in 61 percent of plans, teachers are fully vested within a year or less.

Nearly all of the charter schools that opted out of the state plan and created alternative plans provided some type of matching contribution to their employees. Of these schools, 80 percent provided a 100 percent match on the employee contribution, up to an established limit. On average, that match for employee contributions was equal to 4.3 percent of a teacher’s salary.

Unlike defined-benefit plans, workers with retirement savings accounts must actively choose to contribute to them in order to save for retirement. Some 71 percent of charter schools report that new teachers are knowledgeable about the school’s alternative retirement-plan offerings. Roughly two-thirds of the alternative plans are optional, while one-third automatically enroll teachers. In interviews, the majority of respondents say their teachers are knowledgeable about and satisfied with their plans, and that their teachers find the plan to be as good as or better than the state pension. However, charter schools did have to spend a significant amount of time educating teachers about the benefits of creating an alternative retirement-savings plan as compared to staying in the state pension system, which was far more familiar for most career teachers.

Looking Ahead

State pension plans that in the 1990s seemed like a good deal for start-up charter schools appear to be far less attractive today. Their financial health remains precarious, and the schools and employees who participate in them have reason to be concerned about promised benefits and the substantial cost of providing them. Our analysis shows that charter schools are increasingly opting out of state plans, especially schools with access to greater administrative capacity and knowledge and thicker labor markets.

Nearly all state pension plans failed to meet their target rates of return in the years following the financial crisis, which has necessitated sharp increases in contributions from employers and employees. But instead of saving for future benefits for current teachers, these stepped-up contributions are typically being used to pay down the unfunded liabilities of the plan. Together with stricter eligibility and vesting rules, that is making pensions a less-appealing prospect for new teachers, and by extension, new charter schools.

However, our interviews with charter schools uncovered a major barrier to innovation: across all five states in our study, charter schools said they often struggle to understand whether or not they should participate in their state’s pension plan. Pension and retirement rules are complex and ambiguous, and navigating these systems is especially challenging for independent charter schools. There is a clear opportunity for advocates and supporters, such as state charter support organizations, to create a shared knowledge base and provide additional resources in this area.

Public school districts are facing twin challenges: maintaining a labor supply of qualified teachers while shoring up the deteriorating system that compensates them.

As promised payouts grow, this could have a dramatic impact on what schools can achieve in the classroom going forward. Fortunately, the autonomy provided to charter schools positions them to lead by example on this and other important issues. As we continue to gather information about

how charter schools innovate in both of these areas, it is important to share this knowledge with the larger public-education system.

Michael Podgursky is professor of economics at the University of Missouri–Columbia. Susan Aud Pendergrass is the vice president of research and evaluation at the National Alliance for Public Charter Schools, where Kevin Hesla is director of research and evaluation.

This article appeared in the Spring 2018 issue of Education Next. Suggested citation format:

Podgursky, M., Pendergrass, S.A., and Hesla, K. (2018). Pensions Under Pressure: Charter innovation in teacher retirement benefits. Education Next, 18(2), 8-15.