Say you’re a 3rd-grade public school teacher with $50,000 in student-loan debt. The federal Stafford Teacher Loan Forgiveness program sounds like a great idea: teach for five years while you make monthly payments right-sized for your income, and the government will forgive $5,000 of what you owe.

But then comes the fine print. Accepting the $5,000 resets a different loan-forgiveness clock—the one that would have erased your outstanding debt entirely after 10 years, since you’re a public employee. To access that benefit, now you’re stuck with another decade of payments, or 15 years in all. It’s hard to follow, and would be even if the explanation were not buried in Section 8 of the “Public Service Loan Forgiveness Employment Certification” form in the third paragraph of the subsection titled “Other Important Information.”

But then comes the fine print. Accepting the $5,000 resets a different loan-forgiveness clock—the one that would have erased your outstanding debt entirely after 10 years, since you’re a public employee. To access that benefit, now you’re stuck with another decade of payments, or 15 years in all. It’s hard to follow, and would be even if the explanation were not buried in Section 8 of the “Public Service Loan Forgiveness Employment Certification” form in the third paragraph of the subsection titled “Other Important Information.”

Welcome to the world of student loans and debt forgiveness for teachers, a patchwork of overlapping programs, contradictory regulations, and expensive subsidies that date back to Dwight D. Eisenhower’s signing of the National Defense Education Act of 1958. This 60-year experiment in using federal loan dollars to encourage students to become teachers could be poised for change as Congress considers reauthorizing the Higher Education Act. There is broad, bipartisan agreement that simplifying the nation’s byzantine student-loan programs is an important goal, which is a good start. But lawmakers must also examine how these programs may have encouraged more teachers to pursue education master’s degrees and driven up their price, and whether loan forgiveness programs actually do what they are supposed to — recruit and retain teachers, to the benefit of students.

A Labyrinth of Loans

On October 4, 1957, the Soviet Union launched the rudimentary satellite Sputnik into low-earth orbit, thus marking the beginning of the “space race.” It was also the dawn of preferential federal student-loan programs to benefit students in critical fields, including teaching. Not only did Congress pass legislation using federal dollars to issue low-interest-rate loans to students in certain subject areas, but borrowers who went on to be teachers could have up to half of that debt forgiven. Lawmakers believed high-quality teachers unburdened by student-loan debt could now fully focus their efforts on educating the next generation of scientists and engineers to defeat the Soviet menace.

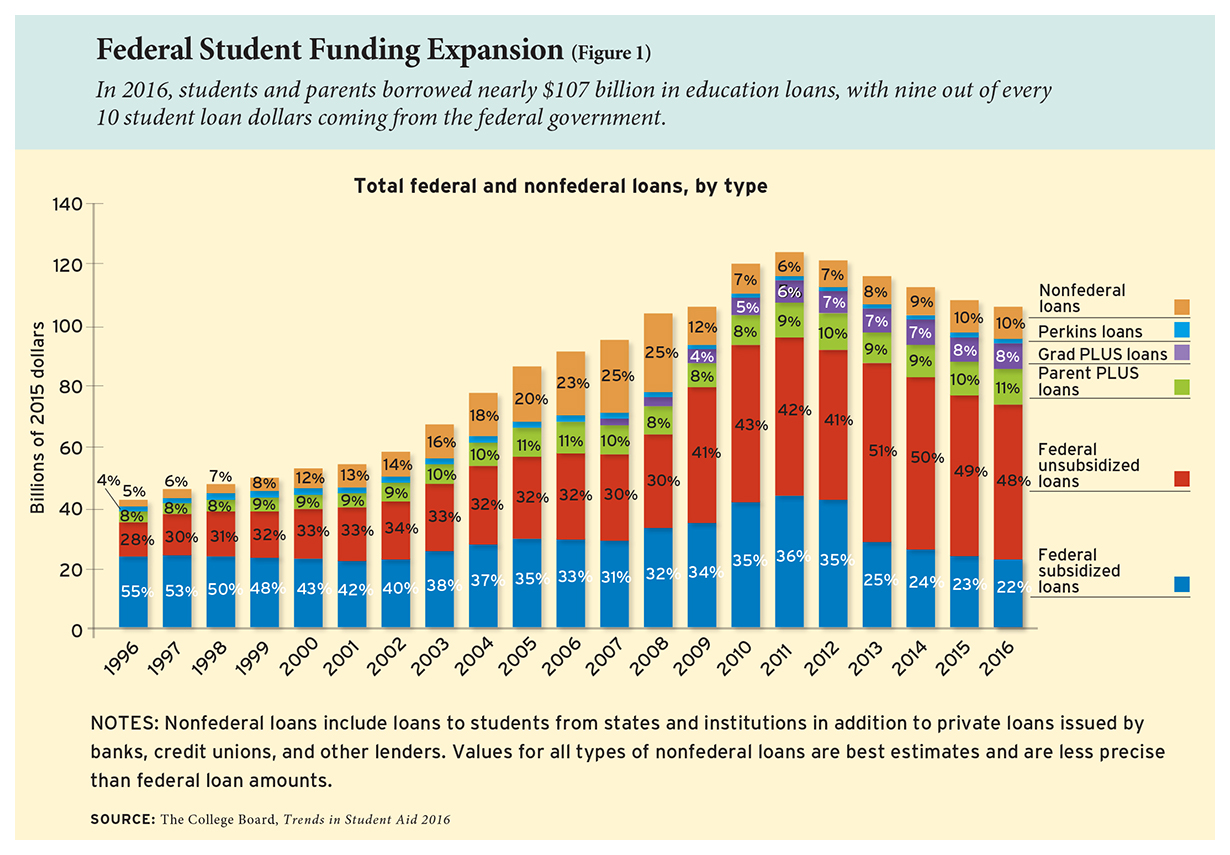

Federal student-aid programs have expanded sporadically in the decades since, and today, 9 out of every 10 student-loan dollars nationwide come from the federal government, totaling $96 billion in 2015–16 (see Figure 1). The borrowing limits and repayment rules are different for each loan program, and many of the terms like interest rates and fees vary as well. Students must fill out a Free Application for Federal Student Aid (FAFSA) form in order to obtain federal loans, but their finances have little bearing on their eligibility.

Students preparing to become teachers are eligible for four different types of federal loans. Through the Stafford Loan program, undergraduates can borrow between $5,500 and $12,500 each year from the U.S. Department of Education, depending on how many years they’ve been in school and whether they are considered financially dependent on their parents. Federal Perkins Loans—the descendants of the original “space race” loans—are also available at some, but not all, colleges and universities, with a combination of federal and institutional support worth up to $5,500 per year. Graduate students may borrow up to $20,500 a year using the Stafford Loan program, after which they may use the PLUS Loan program, which provides loans up to the cost of attendance, calculated as tuition plus living expenses.

In addition, federal TEACH Grants of up to $4,000 each year are available to aspiring teachers. While called “grants,” the funds come with complex strings attached and ultimately function more like loans. To avoid repayment, recipients must teach in a high-need field in a low-income school within one year of graduation, and spend four of the next eight years in that or a similarly qualifying role. The U.S. Department of Education estimates that 74 percent of recipients will not meet those requirements and be required to repay their “grant” in full, with accrued interest dating back to the day the funds arrived.

In addition, federal TEACH Grants of up to $4,000 each year are available to aspiring teachers. While called “grants,” the funds come with complex strings attached and ultimately function more like loans. To avoid repayment, recipients must teach in a high-need field in a low-income school within one year of graduation, and spend four of the next eight years in that or a similarly qualifying role. The U.S. Department of Education estimates that 74 percent of recipients will not meet those requirements and be required to repay their “grant” in full, with accrued interest dating back to the day the funds arrived.

Students preparing to be teachers access these programs in various ways. To get a sense of how much student-loan debt teachers accrue, on average, we look at federal loan data from the 2011–12 school year for undergraduate students who majored in education, who account for approximately 9 out of 10 students in traditional teacher-training programs nationwide. Graduates of those programs comprise about 70 percent of U.S. teachers.

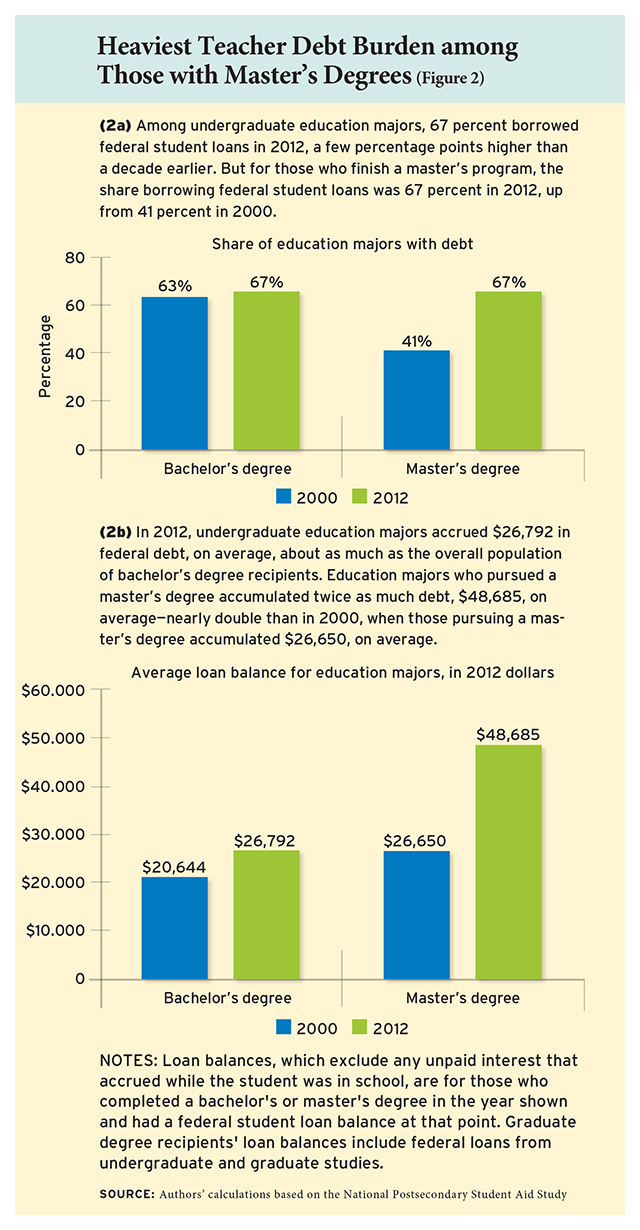

Among undergraduate education majors, some 67 percent borrowed federal student loans—5 percentage points more than the overall population of bachelor’s degree recipients (see Figure 2). They accrued about as much federal debt, at $26,792, on average. Some 13 percent had Perkins Loans, with an average debt of $3,142. In addition, about 30,000 students nationwide receive TEACH Grants each year, worth $2,881, on average.

Teachers who go on to pursue master’s degrees accumulate significantly more debt. In 2011–12, 59 percent of students who completed master’s degrees in education borrowed federal loans for graduate school and accumulated $37,750 each, on average, from their graduate studies alone. In all, 67 percent of students who finished a master’s program in education carried student-loan debt from their undergraduate and graduate degrees, owing $48,685, on average.

A Maze of Forgiveness Programs

If navigating four different types of loans was not confusing enough, teachers may qualify for as many as four different loan-forgiveness programs passed by Congress in fits and starts over the past two decades.

Since its space-race inception, the Perkins Loan program has offered generous loan-forgiveness terms for teachers. Borrowers who work in a low-income school or in subject areas their state designates as in critical need, such as math and science, qualify to have a percentage of their Perkins debt canceled each year for five years until all of the debt is forgiven. But the generous nature of this benefit is limited, since few teachers have these loans and those who do tend to have low balances. Unlike every other forgiveness program, Perkins borrowers apply for forgiveness through their school rather than the federal government.

The limited availability of the Perkins program is partly what prompted Congress to create the Teacher Loan Forgiveness program for the more widely available Stafford Loans in 1998. Like the Perkins program, borrowers need either to teach high-need subjects or in schools serving predominantly low-income students. However, $5,000 of their Stafford debt is canceled in a lump sum after five consecutive years of monthly payments. Certain teachers can have even more debt forgiven: in 2004 and 2006, Congress increased the loan-forgiveness benefit to $17,500 for teachers in math, science, and special education.

Congress acted again in 2007 to provide more loan forgiveness, creating the TEACH Grant program for teachers and the Public Service Loan Forgiveness Program (PSLF), which benefits teachers and other public employees. Under that program, all outstanding student-loan debt is forgiven after 10 cumulative years of monthly payments while the individual is working in any federal, state, local, tribal, or 501(c)(3) nonprofit job.

Also in 2007, lawmakers passed legislation to decrease the amount workers had to pay each month. Through the Income-Based Repayment (IBR) program, monthly student-loan debt payments were capped at 15 percent of income beyond a large exemption. Three years later, that program was made more generous, with a 10 percent cap. The more-generous IBR program and PSLF are only applicable to Federal Direct Loans, as opposed to older Federal Family Education Loans, which were more costly to the government and were phased out in 2010. However, because of this technicality, in order to take advantage of these generous new payment and forgiveness programs, borrowers with older loans often need to consolidate them.

The piecemeal expansion of these programs over time reflects political expediency and the government’s efforts to wring inefficiencies out of the loan program. Under the old Federal Family Education Loan program, the government relied on private lenders to make most government-backed loans; as the government began to cut lenders’ subsidies in the 1990s and beyond, eventually moving to all direct lending in 2010, lawmakers had extra funds on their hands.

While lawmakers could have used those savings for anything, teacher loan forgiveness was an attractive option. Reallocating savings to other programs is more politically popular than reducing spending, so deficit reduction was always unlikely. But procedures and practices in Congress make it difficult to reallocate spending to just any government program—it’s much easier to reallocate those funds within the same agency or even the same set of programs.

Thus, Congress kept the savings in the federal student-loan program but shifted the funds from private lenders to teachers—a move hardly any politician could oppose. With each major change, lawmakers created a new forgiveness program without eliminating the old ones, unwilling to risk some subset of teachers losing out.

Competing Rules

The benefits from loan-forgiveness and income-based repayment programs can add up. For a teacher earning the average starting salary of $36,141 with a typical undergraduate loan balance, enrolling in an income-based plan would save her as much as $200 a month: she’d pay $100–150, compared to $300 under the standard 10-year repayment plan. And because those lower payments cover little more than the accruing interest, with the forgiveness plan, after 10 years, most of her principal balance remains and will be forgiven.

That’s if she follows the right sets of rules at the right times, however. These programs are difficult to navigate and access, with competing sets of rules that affect borrowers in ways that are hard to predict. Loan-forgiveness programs do not automatically kick in once the requirements are met. Borrowers must re-enroll in income-based plans every year, track each loan type against the applicable loan-forgiveness qualifications, and submit paperwork to the federal Department of Education, or, in the case of Perkins, to the college they attended. And not only do the programs fail to work together well, they can contradict one another. At this point, the public-service forgiveness program is almost always the best option, making the older forgiveness programs developed specifically for teachers more like potential traps than benefits.

For example, Perkins Loans are not eligible for the income-based repayment plans unless the borrower consolidates the loans with her other federal student loans. But if she does that, her Perkins Loans lose eligibility for forgiveness under the Perkins program. If a teacher wants to maintain that benefit but repay her other loans under an income-based plan to qualify for public-service loan forgiveness, she’ll have to be sure she is paying off her Perkins Loan separately.

Then there is the Stafford Teacher Loan Forgiveness program. Teachers who take advantage of it after five years of payments, which gets them $5,000 to $17,500 in forgiveness, disqualify those years of payments from counting toward the Public Service Loan Forgiveness program, which forgives all outstanding debt at year 10.

Add to that the TEACH Grants, which automatically transform to loans, with back interest due, if teachers fail to hew to all of the rules. Meanwhile, teachers don’t make payments on these grants unless and until they convert to a loan, which can have dramatic and unintended side effects on loan forgiveness. Because the teacher does not make payments on them while they are grants, she is not accruing years of payments toward public-service loan forgiveness.

Say a teacher has $10,000 in TEACH Grants and another $50,000 in federal loans. After one year teaching in a high-needs school, she takes a job in a non-qualifying school nearby for the next four years. All the while, she has been making income-based payments on her $50,000 in loans, and at year five, is halfway toward receiving public-service loan forgiveness.

But in that fifth year, the TEACH Grants automatically convert to loans, because it has become impossible for her to meet the length-of-service requirement to teach at a high-needs school. Now she owes an additional $10,000 in student-loan debt, plus at least $2,000 in interest, and is facing 10 more years of payments before forgiveness. If she had instead opted to convert the TEACH Grants to a loan in year one, she would have avoided that problem and made only 10 years of payments. And even though her debt amount would have been greater, her payments would have remained the same, because the monthly bill is based on income, not debt. The “grant” money will cost her five additional years in income-based payments—years in which her income is growing, so her monthly debt-repayment bills will as well.

For Graduate School, the Sky’s the Limit

Another surprising side effect of loan forgiveness and income-based repayment programs is an explosion in teachers pursuing expensive graduate degrees—for free. Federal rules mean that taxpayers foot the bill, not teachers.

If a teacher with a master’s degree goes on to earn the median teacher’s salary in the U.S., even after making 10 years of income-based payments, she won’t have paid back more than the first $17,000 in federal student loans she borrowed as an undergraduate before the remainder of her debt is erased. Every dollar she borrowed for graduate school—which under federal rules can include living expenses—ends up being “free” (i.e., forgiven). That investment might be worthwhile if master’s degrees produced better teachers. However, an overwhelming amount of research has shown that teachers who have a master’s degree are no more effective, on average, than those who do not.

Yet our national investment in these programs is growing: more teachers are earning master’s degrees and amassing more student-loan debt to cover the costs. The percentage of teachers with a master’s degree grew from 42 percent in 2000 to 48 percent by 2012, while teacher salaries, adjusted for inflation, have been flat since 2004 (see Figure 3).

In 2000, 41 percent of master’s of education recipients had federal loans with an average balance of $26,650, including undergraduate and graduate school debt. By 2012, after the implementation of Grad PLUS and the promise of unlimited forgiveness, borrowing rates were up to 67 percent of students and the total average debt jumped by more than 80 percent, to $48,685. Compare that with students seeking a master’s in business administration: among students with loans, the average debt grew by only about 10 percent, from $40,839 in 2000 to $44,219 in 2012. You read that right: teachers now leave graduate school with about as much federal debt as MBAs.

Complicated and generous loan-forgiveness programs might be worth it if there were some evidence that loan forgiveness, rather than other interventions, is the best policy approach. In fact, there has never been a clearly stated rationale for loan forgiveness and there are no rigorous studies showing that it helps recruit or retain teachers. These programs are instead a politically convenient response to budgetary surpluses in the federal student-loan program, accounting rules, and turf wars between congressional committees. This pattern has repeated itself throughout the history of federal financial aid for higher education. It’s why the system is so complicated now, and why it’s so hard to reform.

A Better Way Forward

If Congress is convinced that the federal government should spend money to boost teachers’ disposable income, capping debt payments and forgiving loans are poor strategies. Subsidizing payments is a roundabout way of subsidizing income. Loan forgiveness does nothing to reduce a teacher’s monthly loan burden and its benefits are back-loaded. Plus, it is an opaque benefit. Teachers will struggle to understand what benefits they qualify for in advance. They might not ever learn about them, and the restrictions on who qualifies will arbitrarily shut out or deter otherwise deserving teachers.

A simpler approach would redirect the money for various loan-forgiveness programs to a federal income-tax credit for teachers. Lawmakers could tailor the tax credit in various ways, such as limiting the number of years teachers could claim it, or limiting eligibility to teachers in schools serving predominantly low-income students. Such credits could do all of the things loan-forgiveness programs are supposed to, such as boost teachers’ pay, offer an incentive to stay in the profession, and transfer federal resources to local schools. And they would free teachers from complicated, competing rules and regulations.

Of course, this would amount to a sizable increase in federal spending for K–12 education, benefiting a specific group of people—teachers. The politics of such investment is uncertain, especially since loan forgiveness and tax credits are the responsibility of different congressional committees. It’s also unclear whether federal intervention to raise teacher pay is desirable, would have a positive effect on retention, and would benefit student learning.

For one thing, money is not the main reason teachers cite for leaving the profession; working conditions are (see “The Revolving Door,” research, Winter 2004). A 2014 National Center for Education Statistics report shows that of teachers who left teaching voluntarily, only 7 percent left due to salary. The biggest reason cited by far was “personal life factors.” And among those who switched between teaching jobs, salary was rarely the biggest reason mentioned. Instead, it was “personal life factors” and “school factors” (otherwise known as “I didn’t like where I worked”).

In order to justify a federal policy to pay teachers more, policymakers would need to prove that higher pay would lead to better teachers and outcomes for students. They would also ideally be able to prove that recruiting better teachers (and thus depleting the labor pool for other careers) is beneficial to society. They would then need to explain why, if teachers are underpaid compared to their societal contributions, the federal government is able to recognize this and act on it but states and local school districts are not. And, finally, they would need to demonstrate that districts won’t simply use federal benefits to supplant planned increases in teacher pay. Perhaps all of the current subsidies baked in through loan forgiveness already are suppressing teacher salaries.

We don’t know the answers to these questions, but neither does anyone else, particularly members of Congress. They have consistently used federal dollars to create programs that benefit a limited group of individuals and institutions of higher education with no evidence that this approach benefits society, or even the targeted individuals. Of particular concern, the dynamics that led Congress to create multiple programs in the first place remain and are likely to work against consolidating the programs now. Simplification will be hard, because someone or some group will almost always end up with a smaller government benefit.

The reauthorization of the Higher Education Act presents an excellent opportunity for policymakers to create a clearer and fairer system with fewer hidden subsidies and perverse incentives. Doing that means asking basic questions, and being prepared for large-scale change. How should federal funds advance our education goals? Is paying for graduate school a sound investment in our nation’s teachers and schools? Do existing loan-forgiveness programs actually work, and how well? Advocates and policymakers must not let the prospective elimination of some programs be the enemy of simplifying and supporting others.

Jason Delisle is a resident fellow at the American Enterprise Institute. Alexander Holt is an independent consultant in Washington, D.C.

This article appeared in the Fall 2017 issue of Education Next. Suggested citation format:

Delisle, J., and Holt, A. (2017). The Tangled World of Teacher Debt: Clashing rules and uncertain benefits for federal student-loan subsidies. Education Next, 17(4), 42-48.