The costs of retiree benefits for educators, including “legacy” costs from unfunded benefits for previous retirees, consume a large and growing share of public spending on K–12 education. Between 2004 and 2012, data on fringe benefits from the Bureau of Labor Statistics show that pension costs for public educators rose from 11.9 to 16.7 percent of salaries. In contrast, pension costs for professionals in private firms were relatively flat, at about 10 percent of salaries, over the same period. These gaps are likely to continue to widen as states and school districts attempt to pay down large unfunded liabilities in educators’ defined benefit (DB) pension plans. Using estimates from the pension funds themselves, the Pew Center on the States estimates that the unfunded liabilities of state and local governments for retirement benefits total roughly $1 trillion. (About half of that is school-related, since K–12 workers represent about half of state and local employment.) That trillion-dollar number, as vast as it seems, understates the seriousness of the situation. Most economists agree that the official calculations greatly underestimate the true liabilities. Estimates of the unfunded liabilities more than double if similar calculations are performed using standard methods in financial economics.

Defined benefit plans provide retirees with a guaranteed lifetime benefit, the annual value of which is typically based on number of years of service and average salary during the final years of their careers. Between 1973 and 2005, the share of private-sector workers covered by DB pensions declined substantially, from 88 to 33 percent, while the share of workers in a defined contribution (DC) plan only, e.g., a 401k or IRA, jumped from 16 to 63 percent. DB plans remain the norm in the public education sector, however, despite the fiscal problems and the weak economic rationale for mobile professionals like teachers, many of whom move out of state or out of the profession and lose much of their accumulated benefits. Furthermore, as a result of pension enhancements enacted during the stock market boom in the 1990s, the role of DB pensions in the total compensation package for public educators has become larger over time. This is a clear area where the public and private sectors are on opposite trajectories.

There are a variety of reasons DB pension plans have persisted in public education. The most obvious factor is strong teacher support. Unquestionably, teachers unions have vigorously advocated for generous DB retirement benefit plans.

A largely overlooked factor is that education administrators, the “stewards” of the system, are enrolled in the same plans as teachers. This is typically not the case in large private-sector firms, where senior managers have their own retirement benefit plans. As we document below, the rule structure in educator pension plans, combined with the career-cycle timing of teachers’ promotions into administrative positions, results in senior management in K–12 education enjoying the largest net benefits from these plans. With such high personal stakes, there is no reason to expect K–12 administrators or the organizations that represent their interests to support pension reform efforts. Yet it is these administrators who are expected to be the professional voice for the school districts that are bearing the heavy cost of employee pension benefits.

Final-Average-Salary DB Plans

The DB pension plans in which virtually all public school teachers and administrators in the United States are enrolled share the same general features. In these plans, the annual retirement payment, or annuity, is based on the product of three variables: years of service, a formula factor, and the “final average salary.” In the state of Missouri, the formula factor is 2.5 percent and the final-average-salary calculation averages the highest three years of earnings. Thus, a teacher with 30 years of experience earns 75 percent of her final average salary upon retirement. She can retire and begin collecting benefits as soon as her age and years of experience sum to 80 (“rule of 80”) or when she has 30 years in the system, whichever is sooner. In addition, there is an “early retirement” option whereby educators can retire with a reduced annuity with as little as 25 years in the system, at any age. Once retired, Missouri educators receive annual cost-of-living adjustments to their pensions up to a lifetime cap of 80 percent of final average salary. The structure of the Missouri system is broadly similar to that in other states.

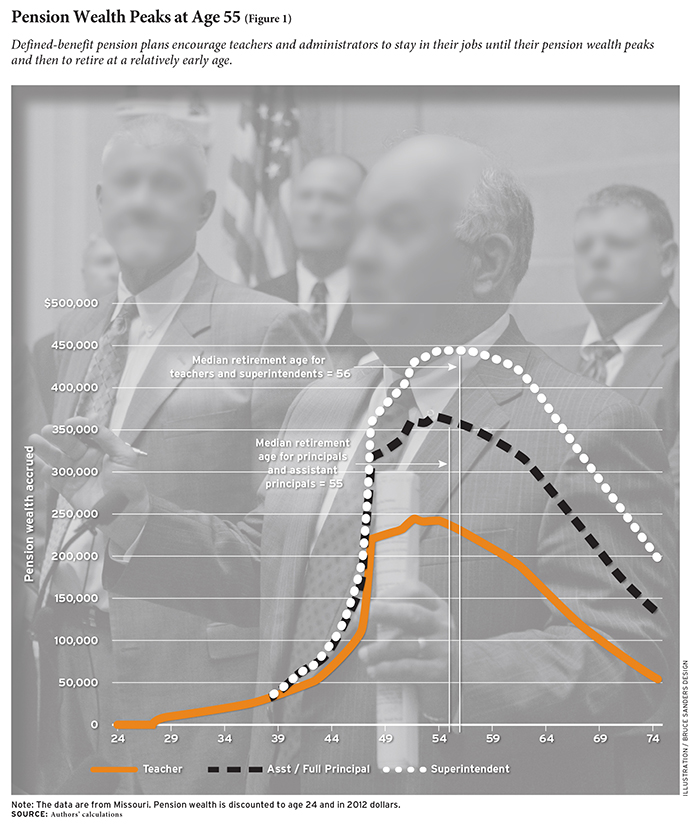

A useful lens for understanding the incentives built into these plans is the rate of “pension wealth” accrual over the career cycle. Pension wealth is the cash value of the expected future stream of pension payments at various points in an educator’s career. The results of such calculations, using standard economic assumptions and actuarial survivor probabilities, are shown in Figure 1, where we plot the growth of pension wealth over the career cycle for a typical educator in Missouri under three different promotion scenarios, in 2012 dollars. In the first scenario the teacher begins teaching at the modal age in Missouri of 24 and remains in the classroom for her entire career. In the second scenario she moves into a principal position. In the third scenario she is further promoted into a superintendent position. The promoted individuals are identical to the baseline career teacher in terms of age at entry into teaching and initial salary; the difference is that they are promoted to these administrative posts at the median promotion age for their respective positions (age 38 for school leadership, age 45 for superintendents). Note that the most common point of entry into principal roles is from teaching, and the most common point of entry into the ranks of superintendent is from principal positions.

As an example of how the pension calculations work, consider a case in which the teacher quits and exits the system at age 35. Using the system’s benefit formula, we can compute the value of the annual annuity payment that she will receive upon retirement under this scenario, which she will be eligible to begin collecting at age 60. The number that we report on the vertical axis in Figure 1 for the age-35 teacher is the dollar value of her stream of annuity payments under this scenario, discounted because she cannot begin drawing payments for many years. Her accumulated pension wealth at age 35 is worth just under $20,000 in present discounted value.

The nearly vertical slope of the pension-wealth accrual curves leading up to age 50 shows the powerful “pull” incentives in these plans, which encourage educators to stay in their jobs. Most of the benefits accrue to educators at the end of a career. Those who quit after 10 or even 20 years amass very little in pension wealth compared to someone who works a full career. Final-average-salary DB pensions are designed to reward longevity, and Figure 1 shows that they are quite effective in this regard. They are also designed to “push” educators into retirement once they reach a certain point in their careers. The push incentive in these plans can be seen in Figure 1 by the negative slope of the pension wealth curve after the peak. Educators working past the peak are doing so for pennies on the dollar. What they gain in current income they lose in the forgone pension they would have been receiving. Not surprisingly, few teachers work for more than a few years beyond the peak.

Administrators as well as teachers are highly responsive to the retirement incentives built into these systems. Note that pension wealth for teachers and administrators peaks around the same time, when educators are in their mid-50s, as shown in Figure 1. The median retirement age (based on Missouri data from 2002 to 2007) is 56 for teachers, 55 for principals, and 56 for school superintendents. These are remarkably young retirement ages for any professional (other than police or firefighters). What is perhaps most striking are the relatively young retirement ages of principals and superintendents, less than one-quarter of whom work into their 60s. It is difficult to think of any private firms, or higher-education institutions, where top and middle management routinely retire at such young ages.

School Administrators

Figure 1 makes it possible to compare career-cycle pension wealth accrual for a teacher to that for a representative principal and superintendent. Pension wealth is higher and more back-loaded for school leaders because their pay is higher than it is for teachers and, crucially, higher at the end of a career. While it is well understood that the final-average-salary DB plans favor long-term teachers over short-term teachers, what seems to have passed largely unnoticed is that that these plans also inherently favor administrators over teachers. Promoted individuals, who have large late-career salary increases, benefit disproportionately from a formula that determines the value of the annuity based on the highest few years of earnings.

Figure 1 reports gross pension benefits by educator type, ignoring the contributions employees make to the pension system over the course of their careers. When we incorporate these contributions into our calculations, administrators fare better still. Promotions create an important disconnect between contributions and benefits. In nearly all educator pension plans (including Missouri’s), teachers and their employers contribute a level percentage of earnings over the course of a career. Thus, during their years of teaching, future superintendents pay into the system a percentage of their teaching salaries, but their benefits years later, after the promotions, are determined entirely by the highest three years of pay, not by lifetime contributions. The reliance of the final-average-salary calculation on just the highest few years of earnings, rather than on lifetime wages (as in Social Security), creates disproportionate returns to late-career promotions.

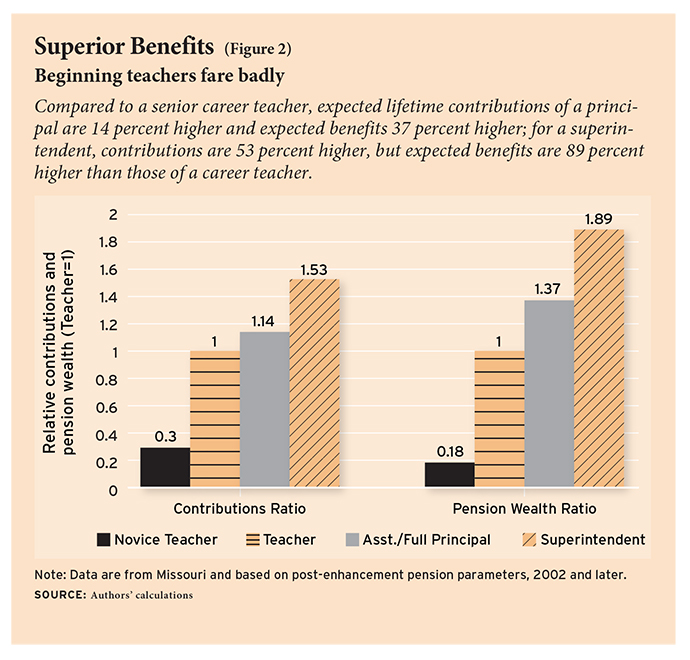

Figure 2 illustrates this point by comparing pension contributions and benefits for “same-vintage” senior teachers, principals, and superintendents, and the much younger novice teachers. The first four bars on the left show relative contributions over the career cycle for each educator type. Contributions for the age 50 teacher with 21 years of system service (the same age and experience level of an average superintendent in Missouri) are normalized to one to provide a common point of comparison. Figure 2 shows that cumulative superintendent contributions are roughly 50 percent higher than those for the same-vintage teacher, with cumulative contributions for the principal falling in between. Not surprisingly, the cumulative expected contributions for the novice teacher are much smaller than for the other groups, owing to the fact that many novice teachers do not remain in the system until the late-career stage.

The four bars on the right report total expected pension wealth, again with the age 50 teacher with 21 years of experience normalized to one. The larger gaps between the bars on the right illustrate the point that pension returns on contributions are larger for school administrators. The expected lifetime contributions of a principal are 14 percent higher than those for a senior career teacher. The expected benefits, however, are 37 percent higher. The lifetime contributions of a representative superintendent are 53 percent higher than those of a career teacher, but expected benefits are 89 percent higher.

Finally, consider the novice teacher. Because of turnover and mobility, this young teacher can expect to contribute 30 percent of what a typical career teacher contributes, but she can expect to collect only 18 percent of the benefits. The math is straightforward and exactly the opposite of that for the administrators. With every paycheck the novice teacher earns, both she and the district make a contribution to a pension system for a benefit far off in the future that she may not collect.

By design, final-average-salary DB pension plans redistribute wealth from young, mobile teachers to career teachers and senior administrators. The problem is that at the individual level there is no link in these plans between contributions and benefits. This type of redistribution is inherent in any plan that bases benefits on the three highest end-of-career years of earnings, while contributions reflect earnings over the entire work life.

Recent Enhancements

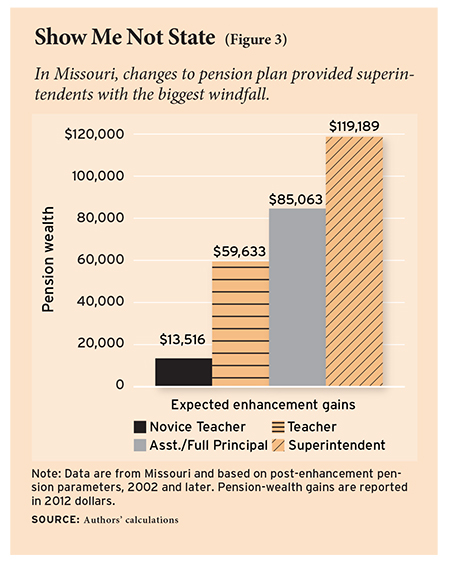

Given that these teacher pension systems back-load benefits, it is not surprising that when enhancements have occurred they have been back-loaded as well. Pension benefits were enhanced greatly in Missouri and many other states during the stock market boom in the 1990s and typically applied retroactively. The fiscal consequences of these enhancements were massive. In Missouri, pension-enhancement legislation produced an immediate windfall in pension wealth across the teaching workforce totaling $1.7 billion (in 2012 dollars). Including potential but yet-unrealized gains raises the estimated cost to more than $3 billion. The distribution of gains in pension wealth associated with the enhancements across the workforce was highly uneven. This fact is illustrated in Figure 3, where we report the estimated gains from the pension enhancements in dollars for the four groups of educators from Figure 2.

Figure 3 shows that school administrators were by far the largest beneficiaries of the enhancement legislation. Moreover, as we outline in separate work, novice teachers were almost certainly made worse off by the enhancements, because several years down the road contribution rates to finance these benefits began to rise sharply.

Figure 3 shows that school administrators were by far the largest beneficiaries of the enhancement legislation. Moreover, as we outline in separate work, novice teachers were almost certainly made worse off by the enhancements, because several years down the road contribution rates to finance these benefits began to rise sharply.

In other words, the pension system, as it works in Missouri and in many other states, transfers wealth from lower-income professionals to higher-income professionals. Novice teachers are subsidizing a handsome payoff to better-paid administrators, who are the appointed guardians of the public interest in the education system.

Conclusion

Retirement benefits represent a large and growing cost for public school systems, as states and school districts struggle to pay down the large unfunded liabilities these plans have produced. Given that these costs put increasing stress on school budgets, it is important to determine whether they can be justified by system benefits. For example, a fundamental question is whether these pension plans improve the quality of the teaching workforce. Studies to date, while few in number, find no positive effects on workforce quality of back-loading pension wealth. It seems likely that schools could do a better job of recruiting young teachers by putting money in upfront salaries rather than in end-of-career pension benefits. But this is an experiment that has yet to be run.

It is widely recognized that teacher quality is the central input in school performance. This insight has put human resource and compensation policies, including performance pay, tenure, alternative route recruitment, and mentoring, at center stage in school reform debates. Some school administrators have been innovators and reform leaders in these areas. Administrator associations have sometimes provided support as well. In the area of teacher pension reform, however, it is important to recognize that school administrators reap the largest net benefits from the current system, which has rising costs and clear inefficiencies. Given the powerful incentives that are in place, there is no reason to expect school administrators or their organizations to support reforms that would provide a more modern and mobile retirement system for young educators, like those found in nearly all other professional employment settings. On the issue of pensions, labor and management are on the same side of the bargaining table.

Cory Koedel is assistant professor of economics, and Shawn Ni and Michael Podgursky are professors of economics at the University of Missouri, Columbia.

For more on this topic, please see “Teacher Retirement Benefits: Even in economically tough times, costs are higher than ever”

This article appeared in the Fall 2013 issue of Education Next. Suggested citation format:

Koedel, C., Ni, S., and Podgursky, M. (2013). The School Administrator Payoff from Teacher Pensions: The “stewards” of the system benefit the most. Education Next, 13(4), 8-13.