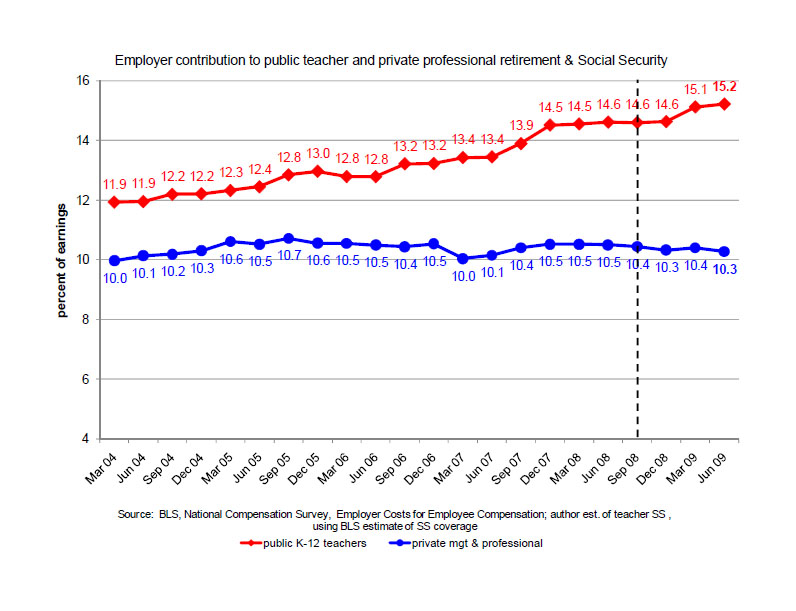

In the Spring 2009 issue of Education Next, Robert Costrell and I presented data on the growing gap between employer pension costs for public school teachers and employer pension costs for private sector managers and professionals. The key chart in that article was a time-series showing pension costs (including Social Security) as a percent of salaries for the two groups. These are computed from the National Compensation Survey, an employer survey on wages and benefits conducted quarterly by the Bureau of Labor Statistics (BLS) of the U.S. Department of Labor. For reasons of sample size, the BLS only began releasing data on public school teachers in March, 2004. The most recent data we reported in the article was from September 2008. We showed that pension benefit costs are significantly larger for public school teachers than for private sector managers and professionals, and that the gap was widening.

This gap continues to widen. We reproduce below an updated time series including the most recent quarterly data (June 2009), which was just released last week. The vertical dotted line shows the end point of the time series reported in our article. In March 2004, pension costs were 1.9 percentage points higher for teachers than for private sector managers and professionals. By September 2008 this gap had more than doubled to 4.2 points, as reported in the article. By June 2009, the gap had grown further still, to 4.9 percentage points. As is readily seen in the graph, the reason for the widening of the gap is increasing pension costs for public school teachers. Retirement benefit costs for private sector managers and professionals have been relatively flat.

As we noted in our article, as large as this gap is, it understates the gap in total retirement benefit costs because BLS does not collect data on retiree health insurance. While most teachers have access to some sort of subsidized retiree health insurance, this benefit has all but disappeared in private sector firms.

The massive unfunded liabilities of teacher pension funds virtually guarantee that these costs will continue to increase for public schools. In addition, some states are also increasing employee contributions to shore up these funds. An important question for school administrators (and taxpayers) is whether these traditional defined benefit pension systems are the best way to recruit, retain, and motivate a high quality teaching workforce.