States and school districts spend more than $50 billion each year on teacher pensions, the keystone in teacher compensation packages. In theory, they provide a generous and secure pot of gold at the end of a teacher’s career, which serves as an incentive to stay on the job. But in reality, they fail to deliver on both of those promises.

We reviewed pension plans and projections in all 50 states, looking specifically at state assumptions about teacher behavior at two inflection points: early career, when they become eligible for minimal pension benefits, and late career, when they become eligible for full pension benefits. Despite the widely held belief that pensions entice teachers to stay on the job, we find that states base the financial health of their plans on the opposite assumption. State projections, based on historical data of teacher behavior, assume that pension eligibility does not encourage early-career teachers to stay on the job, and that pension rules push most veterans to leave as soon as they reach retirement age.

States’ own assumptions show that on average, more than half of teachers do not receive any employer pension benefits because they leave before they are eligible. Just one in five stays on the job long enough to receive full benefits at retirement. At the same time, the plans’ unfunded liabilities mean that 70 percent of contributions go toward debt payments, not future benefits. While plans rely on all teachers contributing to the pension plan, they count on only having to pay full benefits to the relatively few veterans who stay in the same field, in the same state, throughout their career. Most teachers are paying into a system that, most likely, will never fully pay them back.

We suggest several steps that states can take to immediately improve their pension systems, such as allowing teachers to become vested more quickly and accrue benefits more gradually. Given the substantial public investment in teacher retirement and the important goals of boosting teacher retention, such improvements are long overdue. There are likely better, more targeted ways to boost teacher retention than through current pension systems.

A Long-Promised Payoff

Nationally, 9 out of 10 teachers participate in a “defined benefit” pension plan, which guarantees a set monthly payment as long as a retiree lives. Unlike defined-contribution plans such as a 401(k), where all contributions go directly into a worker’s account, traditional teacher pensions deliver fixed benefits based on formulas that rely on years of service and salary in the final few years before retirement. Teachers generally accept lower base salaries in exchange for future pension benefits, and the plans are funded in part through contributions that are considered part of their pay packages.

Nationally, 9 out of 10 teachers participate in a “defined benefit” pension plan, which guarantees a set monthly payment as long as a retiree lives. Unlike defined-contribution plans such as a 401(k), where all contributions go directly into a worker’s account, traditional teacher pensions deliver fixed benefits based on formulas that rely on years of service and salary in the final few years before retirement. Teachers generally accept lower base salaries in exchange for future pension benefits, and the plans are funded in part through contributions that are considered part of their pay packages.

Such plans are expensive: roughly 1 in 10 dollars spent on education nationwide goes toward teacher retirement benefits. Pension contributions amount to 17 percent of a teacher’s salary, on average, or more than $1,100 per student nationwide (see Figure 1). Those amounts have grown sharply in recent years to historic highs, and contributions to teacher pensions are higher than in any other profession.

These types of pension plans do offer teachers some advantages. While they’re working, teachers don’t have to save for retirement or worry about investing those savings, because the state takes care of all of those decisions. Teachers also don’t have to worry about outliving their pensions, because the state guarantees regular payments until death.

Defenders of the defined-benefit structure also argue that it can encourage teachers to enter and remain in the profession over the long term, because to maximize their future pension wealth, they must accrue the maximum years of service and reach the top of their district’s pay scale. In a typical teacher pension plan, retirement wealth accumulates over time and is tied closely to a teacher’s average salary in her last few years on the job (see Figure 2).

In order to qualify for at least a minimum pension, teachers must first work and pay into the plan for a minimum number of years, called a “vesting” period. Prior to vesting, teachers can withdraw their own contributions, sometimes with interest, if they leave their jobs. But they forfeit any contributions their school or state has made on their behalf.

In order to qualify for at least a minimum pension, teachers must first work and pay into the plan for a minimum number of years, called a “vesting” period. Prior to vesting, teachers can withdraw their own contributions, sometimes with interest, if they leave their jobs. But they forfeit any contributions their school or state has made on their behalf.

Once a teacher reaches the vesting point, she becomes eligible to collect a minimum pension when she reaches the state’s “normal retirement age.” Because her pension will be based on her salary when she quits working, not when she retires, there is only a small incentive associated with vesting. She’ll qualify for at least some retirement benefit if she leaves mid-career, but receiving more substantial retirement benefits requires staying on the job for the long haul. Even 15 or 20 years in, pension benefits for teachers are relatively small.

Then comes year 25 (or 30, depending on the state), when the value of a pension soars. At this point, a teacher’s salary has climbed the final few, steep steps on the pay scale: she is most likely at her “normal retirement age” and her pension benefits peak. This creates the potential for an incentive that cuts two ways, both of which are unhelpful to schools and educational quality.

First, pension rules can encourage the wrong teachers to stay. Poor-performing or burnt-out teachers who are a few years away from maximizing their future pension benefits are unlikely to leave the classroom if staying on means a far more generous pension. In the typical pension plan for a teacher who begins at age 25, retirement benefits double between age 53 and 60. For these teachers, leaving the classroom means leaving a substantial pot of money on the table.

Second, pension rules can also encourage the wrong teachers to leave. Excellent veteran teachers may want to continue working past year 25 or 30, but the value of their pensions stop growing past that point. By staying on, they postpone withdrawing benefits and ultimately reduce the total value of their pension. This push-out feature is unique to defined-benefit plans; by contrast, retirement plans like a 401(k) continue to grow for each year of work, and do not have these sorts of retirement incentives. In this case, the choice to continue working is a choice to lose out on total retirement wealth.

But how does this work in the real world? Do teachers make different decisions about staying or leaving their jobs based on how that might affect their retirement?

Early Career: The Vesting Point

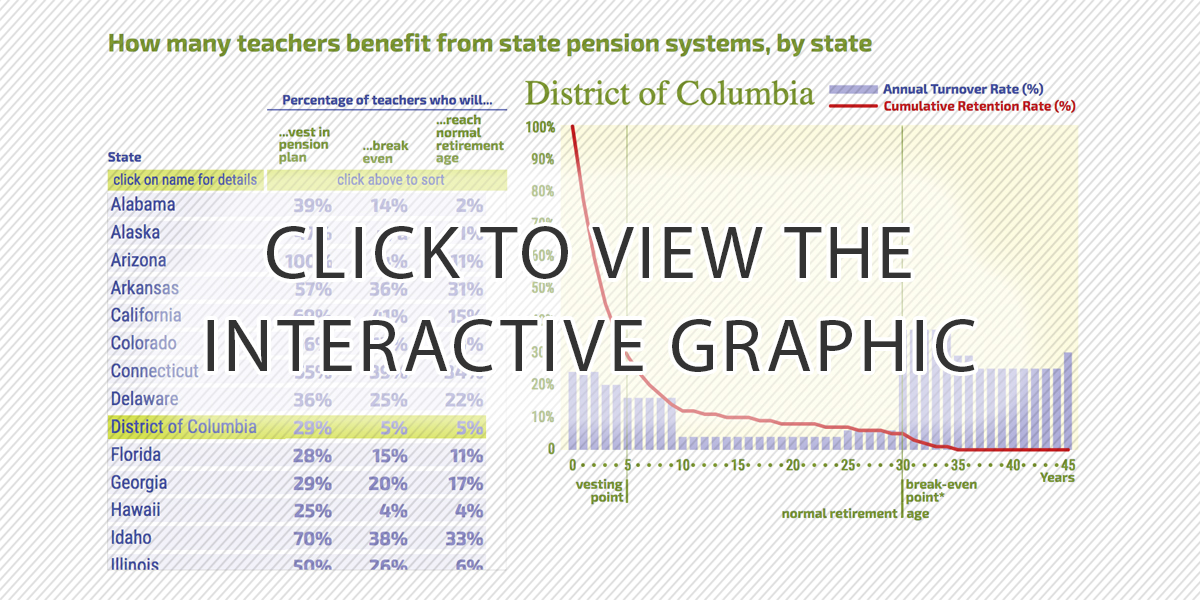

We first look at early-career teachers’ behavior when they become vested in their state’s pension plan, by reviewing state assumptions about teacher withdrawal rates. Each state pension plan publishes a Comprehensive Annual Financial Report (CAFR), which includes withdrawal rate tables that estimate the percentage of teachers who will leave the system before they are eligible for normal retirement. These rates reflect each state’s predictions for the future, and states update them regularly based on historical patterns. Teachers who leave the system before they are vested can withdraw their contributions but lose out on any contributions that the state has made into the system on their behalf.

If vesting were an incentive to keep teachers on the job, withdrawal rates should flatten out in years leading up to the vesting requirement, and then spike upward, at least somewhat, immediately after the threshold. For example, in a state where teachers vest at Year 5, teachers in their fourth year should be less likely to leave their jobs, and those wanting to leave would do so soon after they qualified for benefits.

We find no evidence of any state assuming teachers will systematically change their behavior according to the applicable vesting requirement. On the contrary, every state bases its financial decisions on the assumption that teachers will ignore it.

In the median state, less than half of all teachers are expected to work long enough to vest in their retirement plan—meaning that despite big spending and promises, less than half of all public-school teachers, on average, will ever receive retirement benefits for their years on the job (see Figure 3). States assume that reaching the vesting point has no discernible impact on teacher turnover; in Iowa, for example, projected turnover rates are actually higher among teachers just before the vesting point than immediately after.

From a broader perspective, this means that our significant investment in pensions is not affecting the retention decisions for large groups of teachers. The state of Florida, for example, assumes that a new, 25-year-old teacher has just a 28 percent chance of staying on the job for eight years, at which point she is vested in the pension system. Vesting periods can vary; about half of states set the vesting point at five years of service, and most of the rest require 10 years of service before teachers are eligible to collect a pension. Only one state—Arizona—allows teachers to vest in their pensions right away.

Regardless of why teachers join the profession or how long they intend to stay, it’s clear that qualifying for a pension is not enough to keep them in it. And as states increasingly rely on early-career teachers for stepped-up contributions to shore up their debt-challenged pension systems, this raises basic questions about fairness and equity in the teaching workforce.

Mid-career: Little Influence

In most professions, as workers settle into the middle stage of their career, turnover rates fall. The same is true for teachers, who become less and less likely to leave the profession every year that they stay on the job. Middle-aged, mid-career workers have developed occupation-specific skills that make a radical job change risky and, thus, unlikely. Although it may be tempting to assume that pension plans play a role in teachers’ falling turnover rates, the evidence from other professions and the academic literature on teacher pensions suggests the low mid-career turnover rates are not necessarily due to pensions.

In order to gauge how pensions affect teacher retention, researchers Cory Koedel and Brett Xiang studied what happened after Saint Louis Public Schools greatly expanded teachers’ pension benefits. In 1999, Saint Louis offered retroactive improvement in pension benefits that cost the city $166 million, or $52,000 per teacher, in 2013 dollars, and promised far more valuable pension benefits for future hires. The small group of working teachers already eligible to retire did delay their retirement by one year in order to qualify for enhanced benefits. But no other group of teachers changed their behavior. That is, the city spent millions of dollars enhancing pension benefits but gained very little.

Similarly, Kevin E. Cahill and colleagues found that when Oregon changed its pension plan, reducing its extremely lucrative benefits to pension values that were merely on par with those of other states, there was no decline in teacher retention. For the vast majority of teachers, the prospect of a pension, no matter its size, does not appear to provide a reason to stay or go.

The same pattern appears in states that either do not offer traditional pension plans or allow teachers to choose between a traditional defined-benefit pension or a more portable defined-contribution retirement plan, in which teachers’ contributions and employer matches can be withdrawn, with some limitations, if they leave. For example, since 2002, Florida has offered new teachers a choice between these two types of plans; those who do not choose are enrolled in the traditional pension plan. A study by Matthew Chingos and Martin West found turnover is higher among teachers who pick the portable account compared to those in the pension plan, but the difference is relatively small and is to be expected, given that those teachers have made an affirmative choice for greater mobility. Another study, by Dan Goldhaber, Cyrus Grout, and Kristian Holden, looked at what happened when the state of Washington placed all new teachers into a “hybrid” retirement plan that combined a less-generous pension with 401(k)-style accounts. They found the change had no effect on teacher turnover rates.

Why don’t pensions inspire more teachers to stay on the job? Teachers who leave the profession point to the demands of the job, a desire to pursue other alternatives, other personal factors, and compensation. Teachers do earn somewhat lower salaries than their similarly educated peers, which is partly justified by their more expensive health and retirement benefits. However, that scenario only works for the teachers who stick around for the duration of their career—and teachers themselves may not view it as a fair trade.

Research suggests that not all spending is equal, with teachers preferring cash today to deferred compensation, like benefits, tomorrow. A study of Illinois teachers by Maria D. Fitzpatrick found that, when given the opportunity to purchase pension credits to boost their benefits, they were only willing to pay 19 cents for a dollar of future compensation.

Late Career: A Push out the Door

Research does reveal one moment in a teacher’s career when pension rules can influence her decision: when she is at, or just about to reach, retirement age. While there’s little evidence pensions are strong enough of a “pull” incentive to keep early and mid-career teachers in the profession, there is reason to believe they are pushing some veterans out. Going back to the Oregon example, under its old, more-generous system, when late-career teachers learned of the large windfall waiting for them, most chose to retire rather than continue to teach. After the state moved to a more modest pension system and decreased this late-career windfall, it lost fewer veteran teachers.

The timing of this push-out moment can vary. Just as states project withdrawal rates for when teachers might leave the system before retirement, they also estimate retirement rates in order to project when teachers will retire and begin collecting benefits. However, unlike vesting periods, which apply universally, most states adjust their retirement ages based on how long a teacher has served. Those rules mean different teachers in the same state may become eligible to retire at very different ages. In Arkansas, for example, teachers can retire with full benefits when they reach age 60 and have at least five years of service, or at any age once they have completed 28 years of service. An Arkansas teacher who begins her career at age 22 and teaches 28 consecutive years could potentially retire with full benefits as young as age 50, whereas others will have to wait until age 60. Some states also allow early retirement, where a teacher can retire at an earlier age but with reduced benefits.

This variability means that retirement ages apply differently for every teacher. But they remain formulaic, in that they’re predetermined by the state based upon age and years of experience, not on individual capacity to teach or personal life circumstances. Moreover, the variability makes it difficult to use state retirement assumptions to show the precise interaction between pension plan rules and a teacher’s retirement decision. For example, Missouri allows teachers to retire with full benefits when the sum of their years of service and age equals 80 (see Figure 4). When researchers looked to see whether teachers responded to this “Rule of 80,” they found a steep acceleration in teacher retirements right at that key juncture (see “Golden Handcuffs,” research, Winter 2010). Teachers can reach the rule of 80 at odd ages, like 53 or 58. The fact that many teachers choose to retire at precisely those points suggests that it is the pension plan pushing their retirement decisions.

This variability means that retirement ages apply differently for every teacher. But they remain formulaic, in that they’re predetermined by the state based upon age and years of experience, not on individual capacity to teach or personal life circumstances. Moreover, the variability makes it difficult to use state retirement assumptions to show the precise interaction between pension plan rules and a teacher’s retirement decision. For example, Missouri allows teachers to retire with full benefits when the sum of their years of service and age equals 80 (see Figure 4). When researchers looked to see whether teachers responded to this “Rule of 80,” they found a steep acceleration in teacher retirements right at that key juncture (see “Golden Handcuffs,” research, Winter 2010). Teachers can reach the rule of 80 at odd ages, like 53 or 58. The fact that many teachers choose to retire at precisely those points suggests that it is the pension plan pushing their retirement decisions.

The other significant difference between vesting and retirement assumptions is the magnitude of the turnover rates. While it’s commonly known that teacher turnover rates are high in the early years, it’s less well known that turnover rates are even higher for teachers nearing retirement eligibility. We find that assumed withdrawal rates in the median state decline from 20 percent in a teacher’s first year of service to 4.5 percent by Year 10. However, when a teacher reaches age 55, the median state assumes a turnover rate of 16 percent. That increases again for teachers age 60–67, with an assumed turnover rate of 20–30 percent. Out of 100 teachers who are still teaching at 55 years old, the median state assumes that 65 will retire by their 60th birthday, and only 8 will remain teaching until they reach age 65. That is sooner than U.S. averages for all workers: the U.S. Social Security normal retirement age for anyone born after 1960 is 67, and the Boston College Center for Retirement Research estimates the national average retirement age at 62 for women and 64 for men.

Pushing workers out at the normal retirement age is a defining feature of all defined-benefit plans (including Social Security), and the ones states offer to teachers are no exception. But as a public policy, we should ask whether a state is capable of picking one retirement age that’s right for all teachers, and whether it’s in the public’s interest to push veteran teachers out of the classroom at all.

Social Security, for example, sets a predetermined retirement age based on when a worker was born, but it also offers financial incentives for workers who want to keep working beyond that point. That’s good for workers who get to keep doing what they love; it’s good for employers, because it means lower turnover costs and higher retention of productive workers; and it’s good for the country, because keeping more workers on the job means higher economic output and higher tax receipts. In contrast, most teacher pension plans have more rigid retirement rules than Social Security and also push out teachers at younger ages. If states adopted teacher retirement plans with less formulaic incentive structures, they would let teachers make retirement decisions that better matched their own unique circumstances.

Pension plans do appear to exert a limited “pull” effect that keeps some late-career teachers on the job as they near retirement. (Remember, most teachers have left before then.) But they exert an even stronger “push” effect that encourages veteran teachers to retire, regardless of their particular interest or ability to continue teaching. When researchers have tried to estimate the cumulative effects of these two incentives, they’ve found that shifting to an alternative retirement plan would actually boost late-career teacher retention (see “Peaks, Cliffs, and Valleys,” features, Winter 2008). This could have real benefits for students, because veteran teachers tend to perform better than a replacement teacher just entering the profession.

Ways to Improve

Current teacher pension plans are neither improving the workforce nor providing teachers with adequate retirement savings. Schools are investing billions of dollars in teacher pensions, but they’re getting little return in the way of retention incentives. Meanwhile, teachers are accepting lower base salaries today in exchange for the promise of future retirement benefits, a promise that only a fraction of teachers will ever realize. That disconnect means current teacher pension plans are not working well for teachers, schools, or students.

There are several different options for teacher retirement benefits that could deliver more equitable benefits on a cost-neutral basis. Well-designed, individual portable retirement accounts (somewhat like a 401(k) plan), hybrid plans that combine traditional pension plans with a 401(k)-like component, or alternative models called cash-balance plans that guarantee a moderate interest rate could all provide sufficient retirement savings while giving teachers greater job flexibility. Such a change would protect any teachers who left, regardless of reason, while still providing sufficient benefits to those who choose to stay for a full career.

Even if they do not adopt wholesale change, there are four steps states could take to immediately improve current teacher retirement systems.

First, states should immediately lower their vesting periods to no more than three years. No state should have a 10-year vesting requirement for teachers. Not only would that be illegal in the private sector, but 10 years is simply too long to ask any worker to wait for a retirement benefit, especially in a profession like teaching, with relatively high turnover rates.

Second, if states wanted to try to make vesting more of a retention incentive, they could offer teachers a “graded” vesting system, where workers are eligible for a growing share of their employer’s retirement contributions over time. Graded vesting does not exist in teacher pension plans today, but it is widespread in the private sector. For example, a teacher might be eligible for 33 percent of the employer contribution after one year, 67 percent after two years, and 100 percent after three years. Although there’s no guarantee this would boost teacher retention—that would still require a strong communication effort on the part of the retirement plan—it would at least ensure that more teachers, regardless of their years of service, had access to some employer-provided retirement benefit.

Three, if states keep their defined-benefit systems, they should at minimum move to a more gradual accumulation of benefits. Current teacher pension plans back-load benefits to the last 5 to 10 years of service, mainly because benefit formulas are based on final average salary calculations that do not adjust for inflation. If states extended those final salary calculations from 3 or 5 years to 10 or 20 or 30 years, pension benefits would accrue more steadily rather than spiking at the very end of a teacher’s career. States should also adjust salaries for inflation, so they don’t treat teachers with the same amount of experience levels differently depending on when they completed their service. This is closer to how Social Security works, and it would spread benefits more equitably across all teachers.

Fourth, and most fundamentally, states should stop trying to use pension plans as a tool to shape their workforce and instead think of them as a source of retirement benefits for a large and important class of workers. A close look at the financial assumptions that undergird their plans shows that the states themselves don’t believe these incentives are effective at retaining teachers; in fact, they count on high rates of teacher turnover in order to balance the books. Focusing instead on offering retirement plans that provide all teachers the opportunity to accrue adequate benefits would be a more realistic and equitable approach.

Such changes could have an immediate positive impact on the profession. Allowing teachers to make retirement decisions based on their own unique circumstances, including their desire to continue working with students no matter their location or age, would enhance the profession and improve retirement security for the nation’s teachers.

Chad Aldeman is a principal at Bellwether Education Partners, where Kelly Robson is a senior analyst.